While the S&P 500 is up 26.5% since April 2025, Grand Canyon Education (currently trading at $210.89 per share) has lagged behind, posting a return of 18%. This may have investors wondering how to approach the situation.

Does this present a buying opportunity for LOPE? Or does the price properly account for its business quality and fundamentals?

Why Does Grand Canyon Education Spark Debate?

Founded in 1949, Grand Canyon Education (NASDAQ: LOPE) is an educational services provider known for its operation at Grand Canyon University.

Two Things to Like:

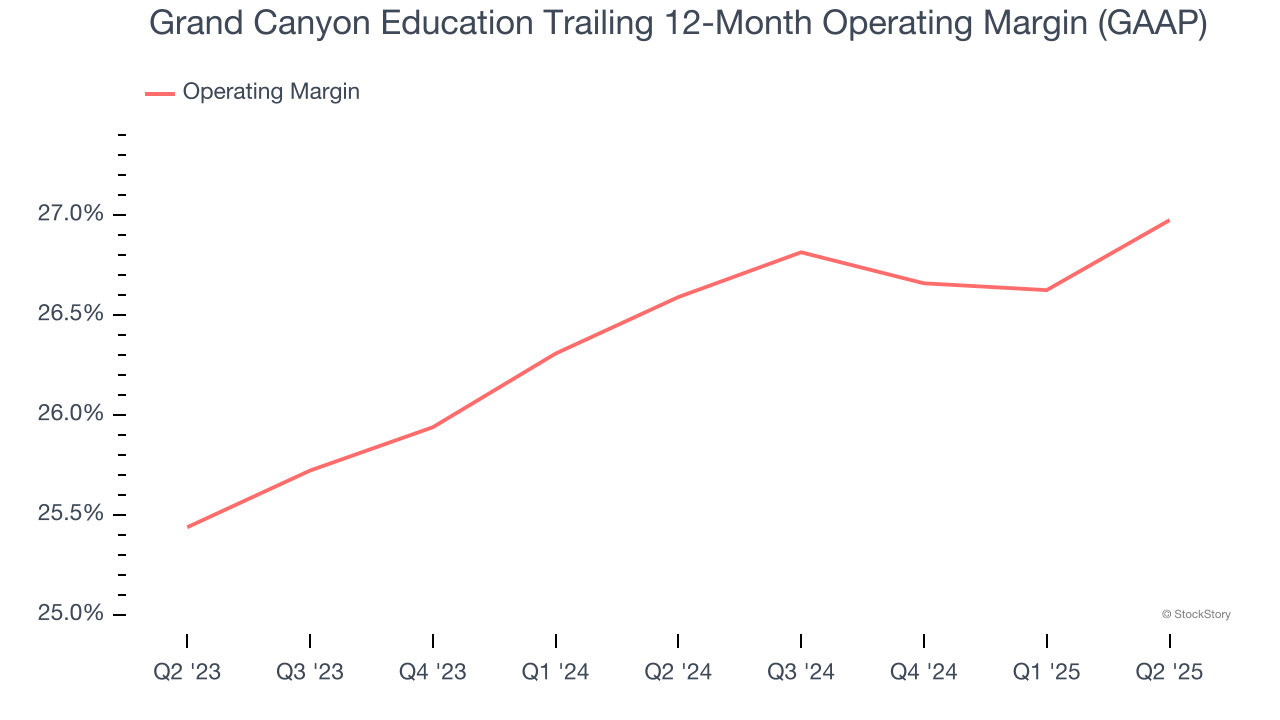

1. Operating Margin Reveals a Well-Run Organization

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Grand Canyon Education’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 26.8% over the last two years. This profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

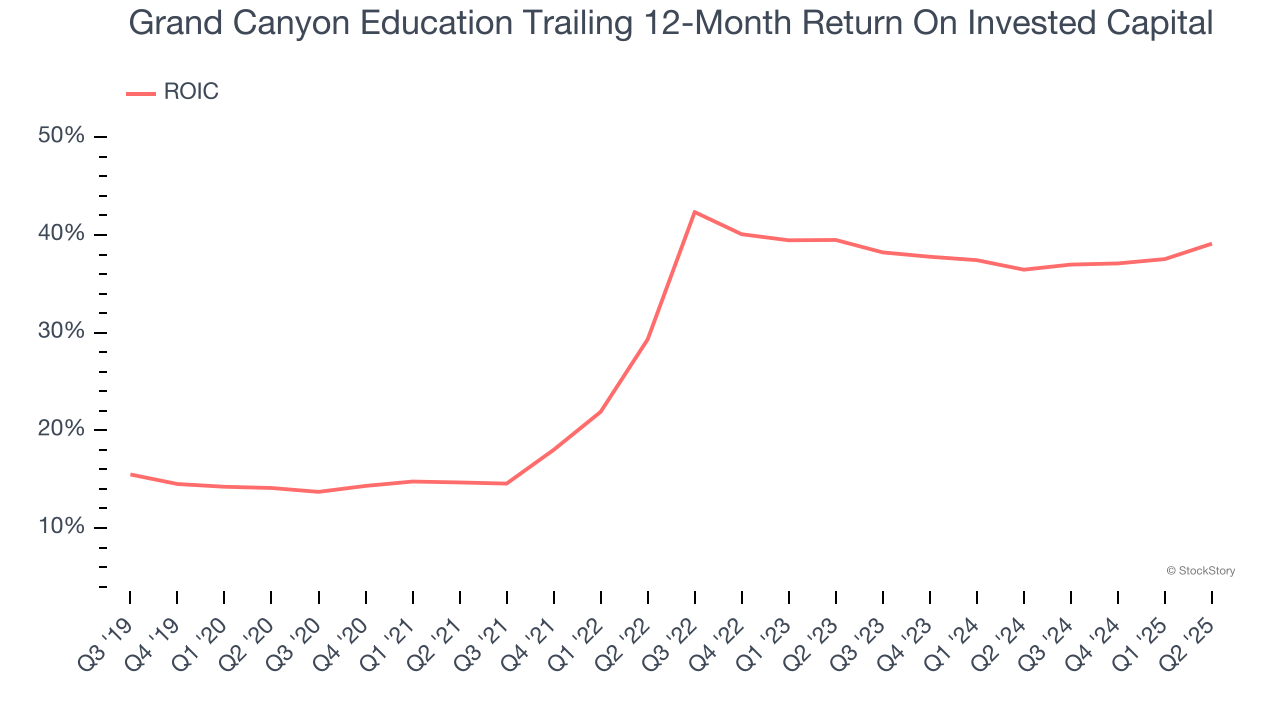

2. New Investments Bear Fruit as ROIC Jumps

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Grand Canyon Education’s ROIC has increased significantly over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

One Reason to be Careful:

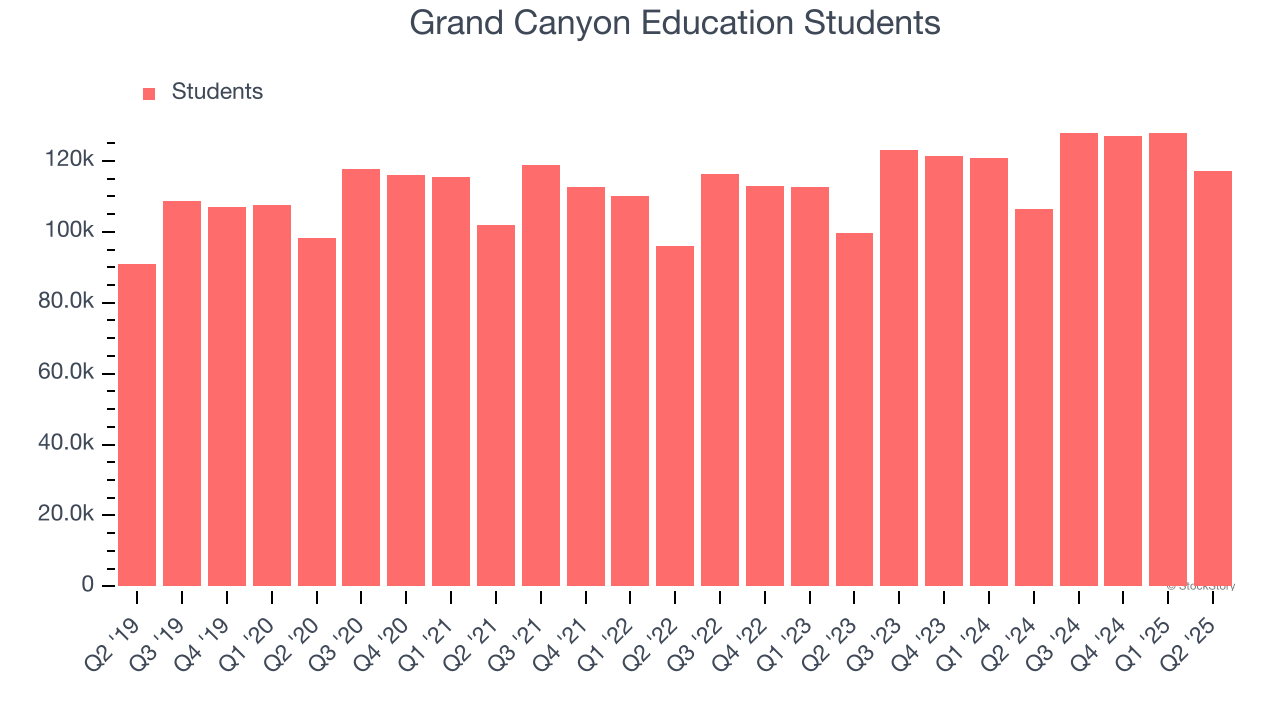

Weak Growth in Students Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like Grand Canyon Education, our preferred volume metric is students). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Grand Canyon Education’s students came in at 117,283 in the latest quarter, and over the last two years, averaged 6.5% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

Final Judgment

Grand Canyon Education’s positive characteristics outweigh the negatives. With its shares underperforming the market lately, the stock trades at 22.4× forward P/E (or $210.89 per share). Is now a good time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

Stocks We Like Even More Than Grand Canyon Education

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.