Although AutoZone (currently trading at $4,028 per share) has gained 12.9% over the last six months, it has trailed the S&P 500’s 26.5% return during that period. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Taking into account the weaker price action, is now a good time to buy AZO? Find out in our full research report, it’s free for active Edge members.

Why Are We Positive On AutoZone?

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE: AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

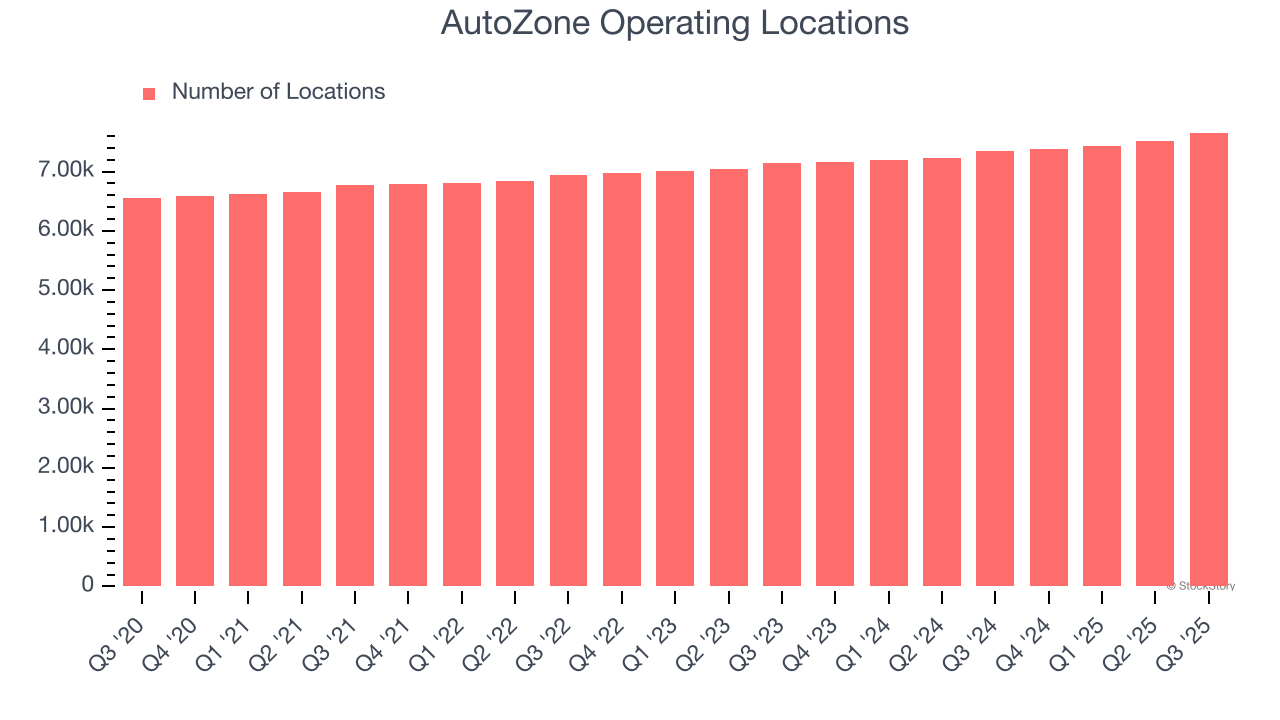

1. New Stores Popping Up Gradually, Supports Growth

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

AutoZone operated 7,657 locations in the latest quarter. It has opened new stores quickly over the last two years, averaging 3.2% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

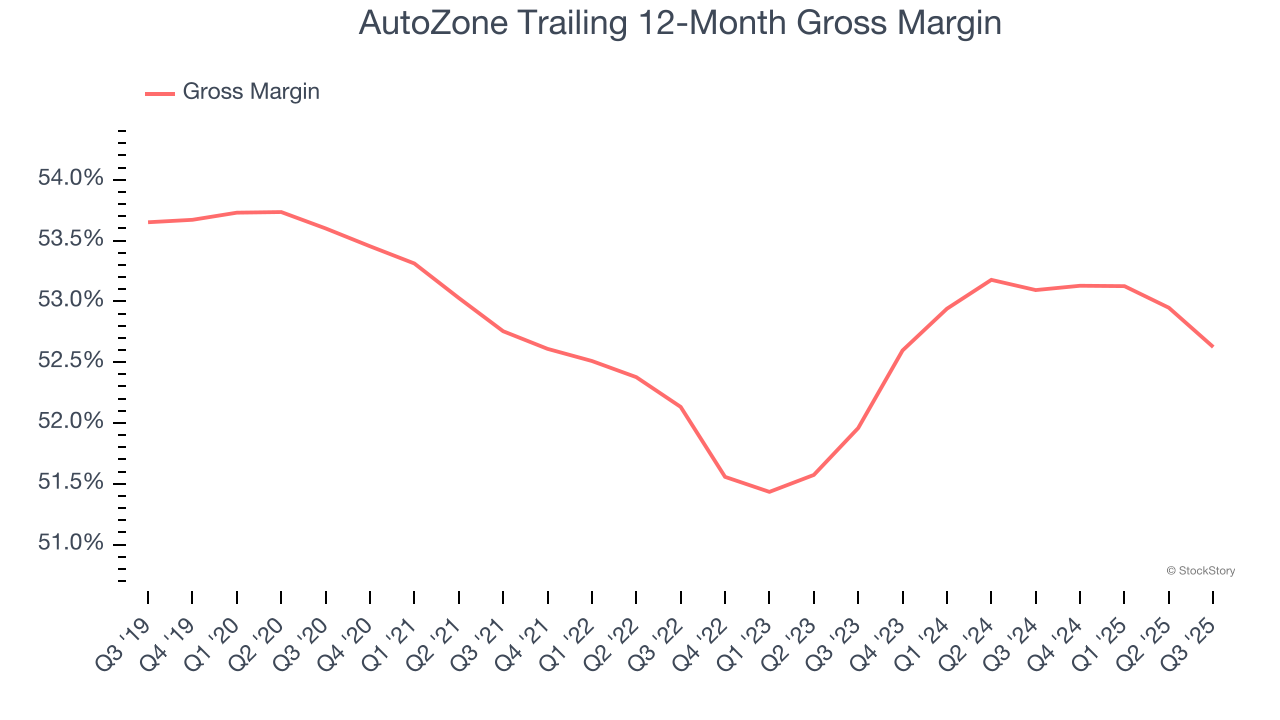

2. Elite Gross Margin Powers Best-In-Class Business Model

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

AutoZone has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent. As you can see below, it averaged an elite 52.9% gross margin over the last two years. That means for every $100 in revenue, only $47.14 went towards paying for inventory, transportation, and distribution.

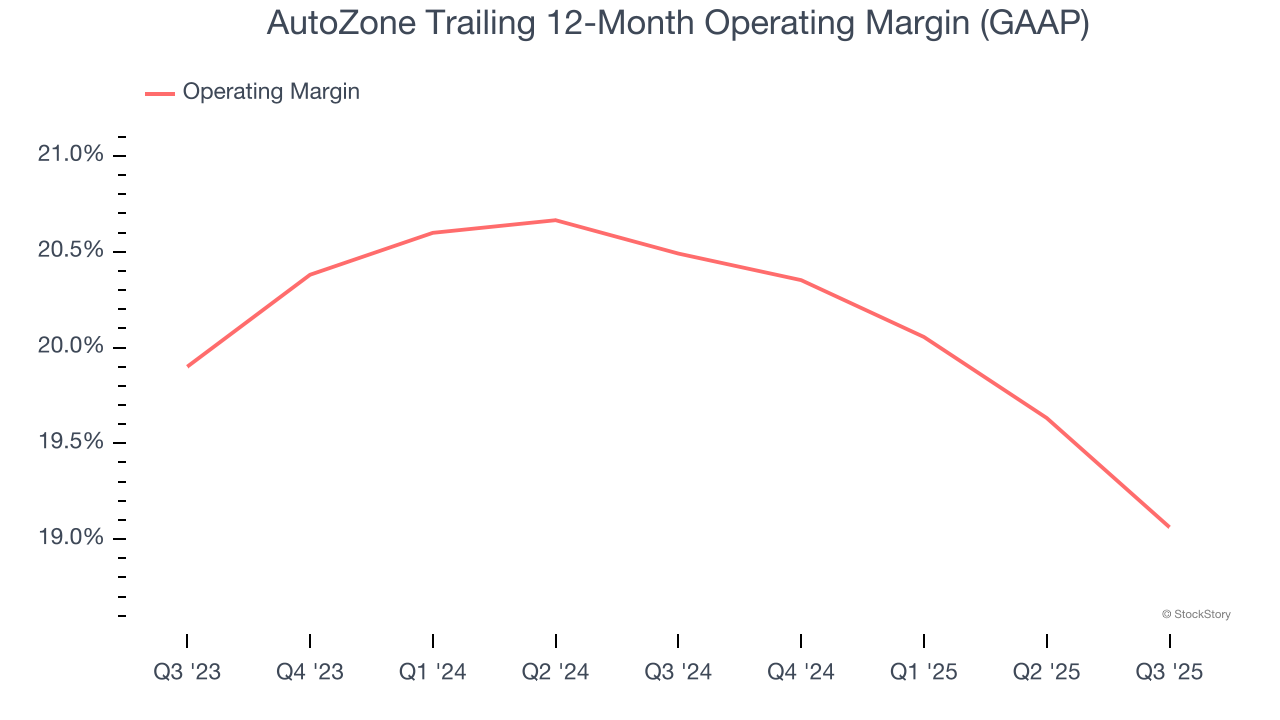

3. Operating Margin Reveals a Well-Run Organization

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

AutoZone has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer retail business, boasting an average operating margin of 19.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Final Judgment

These are just a few reasons AutoZone is a rock-solid business worth owning. With its shares lagging the market recently, the stock trades at 26.1× forward P/E (or $4,028 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free for active Edge members.

Stocks We Like Even More Than AutoZone

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.