Over the past six months, PennyMac Mortgage Investment Trust’s shares (currently trading at $12.05) have posted a disappointing 5% loss, well below the S&P 500’s 26.5% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in PennyMac Mortgage Investment Trust, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Is PennyMac Mortgage Investment Trust Not Exciting?

Even though the stock has become cheaper, we're swiping left on PennyMac Mortgage Investment Trust for now. Here are three reasons we avoid PMT and a stock we'd rather own.

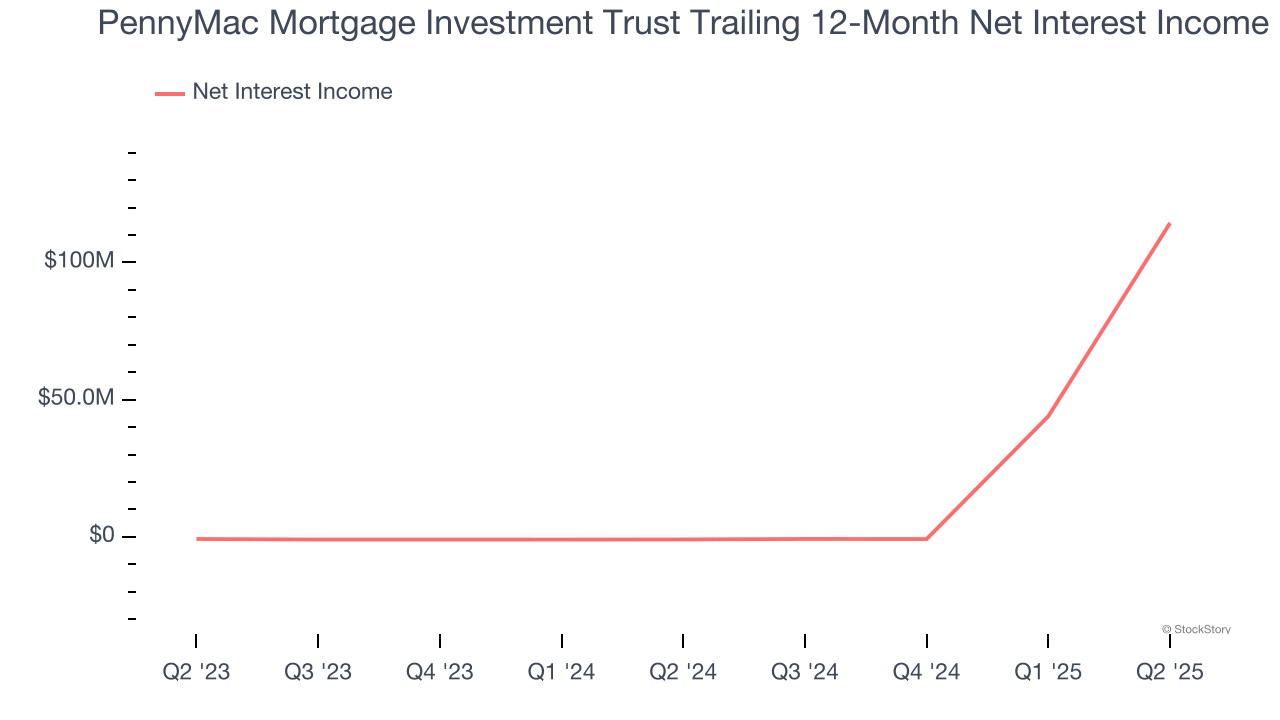

1. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

PennyMac Mortgage Investment Trust’s net interest income has grown at a 3.5% annualized rate over the last five years, worse than the broader banking industry.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect PennyMac Mortgage Investment Trust’s net interest income to drop by 127%, a decrease from its 30.5% annualized growth for the past two years. This projection is below its 30.5% annualized growth rate for the past two years.

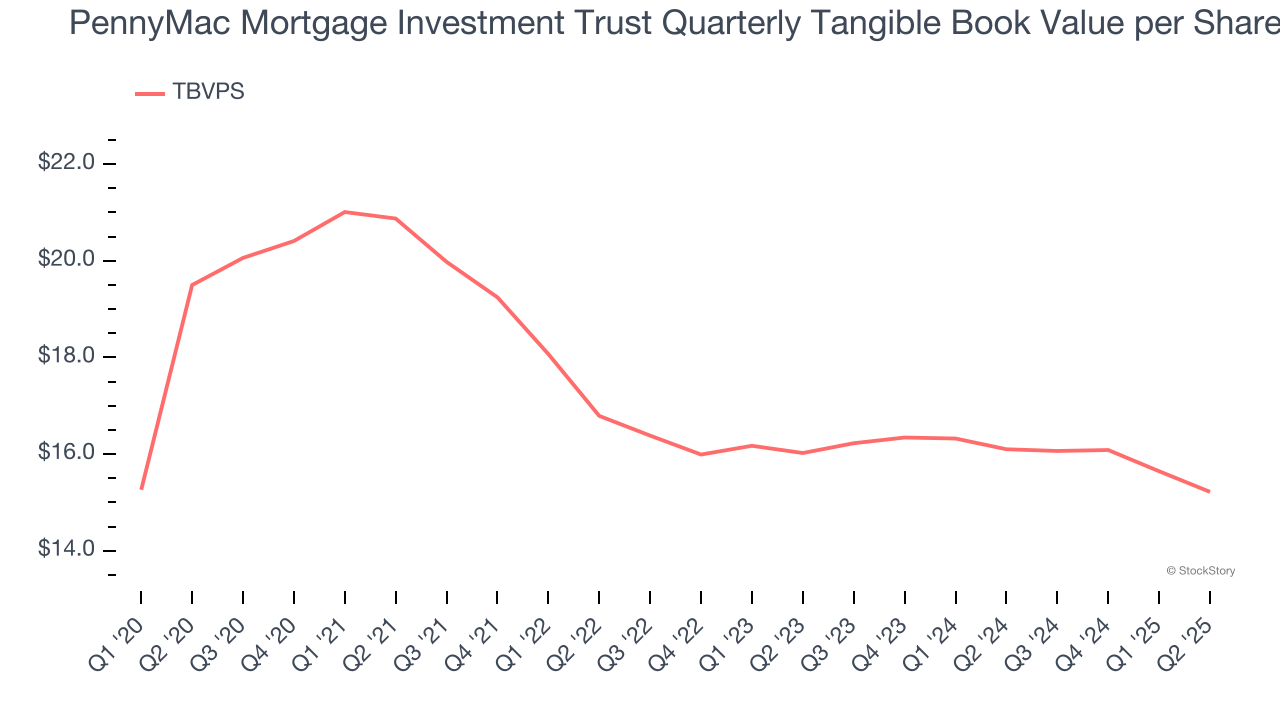

3. Declining TBVPS Reflects Erosion of Asset Value

We consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation.

Disappointingly for investors, PennyMac Mortgage Investment Trust’s TBVPS declined at a 2.5% annual clip over the last two years.

Final Judgment

PennyMac Mortgage Investment Trust’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 0.8× forward P/B (or $12.05 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

High-Quality Stocks for All Market Conditions

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.