Automotive retailer Lithia Motors (NYSE: LAD) announced better-than-expected revenue in Q4 CY2024, with sales up 20.2% year on year to $9.22 billion. Its non-GAAP profit of $7.79 per share was 8.2% above analysts’ consensus estimates.

Is now the time to buy Lithia? Find out by accessing our full research report, it’s free.

Lithia (LAD) Q4 CY2024 Highlights:

- Revenue: $9.22 billion vs analyst estimates of $9.03 billion (20.2% year-on-year growth, 2.2% beat)

- Adjusted EPS: $7.79 vs analyst estimates of $7.20 (8.2% beat)

- Adjusted EBITDA: $419 million vs analyst estimates of $414.7 million (4.5% margin, 1% beat)

- Operating Margin: 4.5%, in line with the same quarter last year

- Free Cash Flow was -$102.8 million compared to -$361.7 million in the same quarter last year

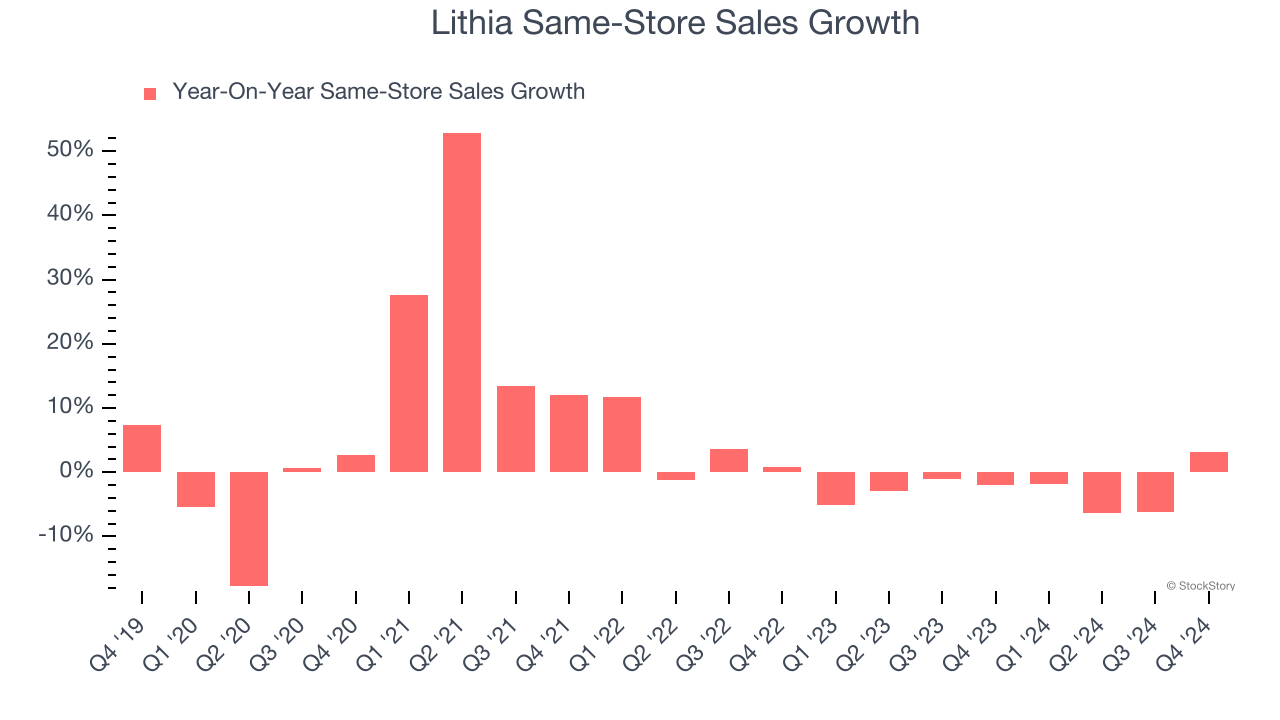

- Same-Store Sales rose 3.1% year on year (-2% in the same quarter last year)

- Market Capitalization: $9.82 billion

"2024 marks another milestone year for Lithia & Driveway, with record-breaking fourth-quarter revenues, the first profitable year for Driveway Finance, and the continued maturity of foundational elements to our strategy." said Bryan DeBoer, President and CEO.

Company Overview

With a strong presence in the Western US, Lithia Motors (NYSE: LAD) sells a wide range of vehicles, including new and used cars, trucks, SUVs, and luxury vehicles from various manufacturers.

Vehicle Retailer

Buying a vehicle is a big decision and usually the second-largest purchase behind a home for many people, so retailers that sell new and used cars try to offer selection, convenience, and customer service to shoppers. While there is online competition, especially for research and discovery, the vehicle sales market is still very fragmented and localized given the magnitude of the purchase and the logistical costs associated with moving cars over long distances. At the end of the day, a large swath of the population relies on cars to get from point A to point B, and vehicle sellers are acutely aware of this need.

Sales Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

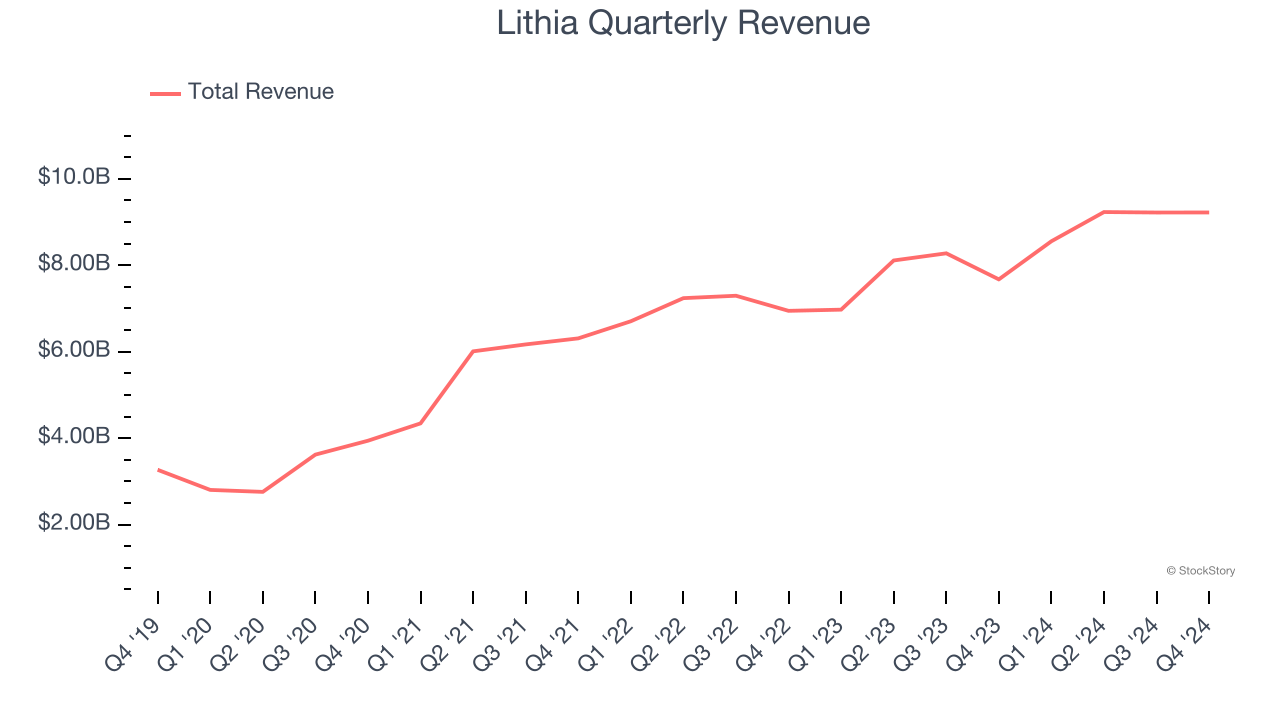

With $36.23 billion in revenue over the past 12 months, Lithia is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences consumer purchasing decisions.

As you can see below, Lithia grew its sales at an incredible 23.4% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as it opened new stores and expanded its reach.

This quarter, Lithia reported robust year-on-year revenue growth of 20.2%, and its $9.22 billion of revenue topped Wall Street estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 8.2% over the next 12 months, a deceleration versus the last five years. We still think its growth trajectory is attractive given its scale and implies the market sees success for its products.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Store Performance

Number of Stores

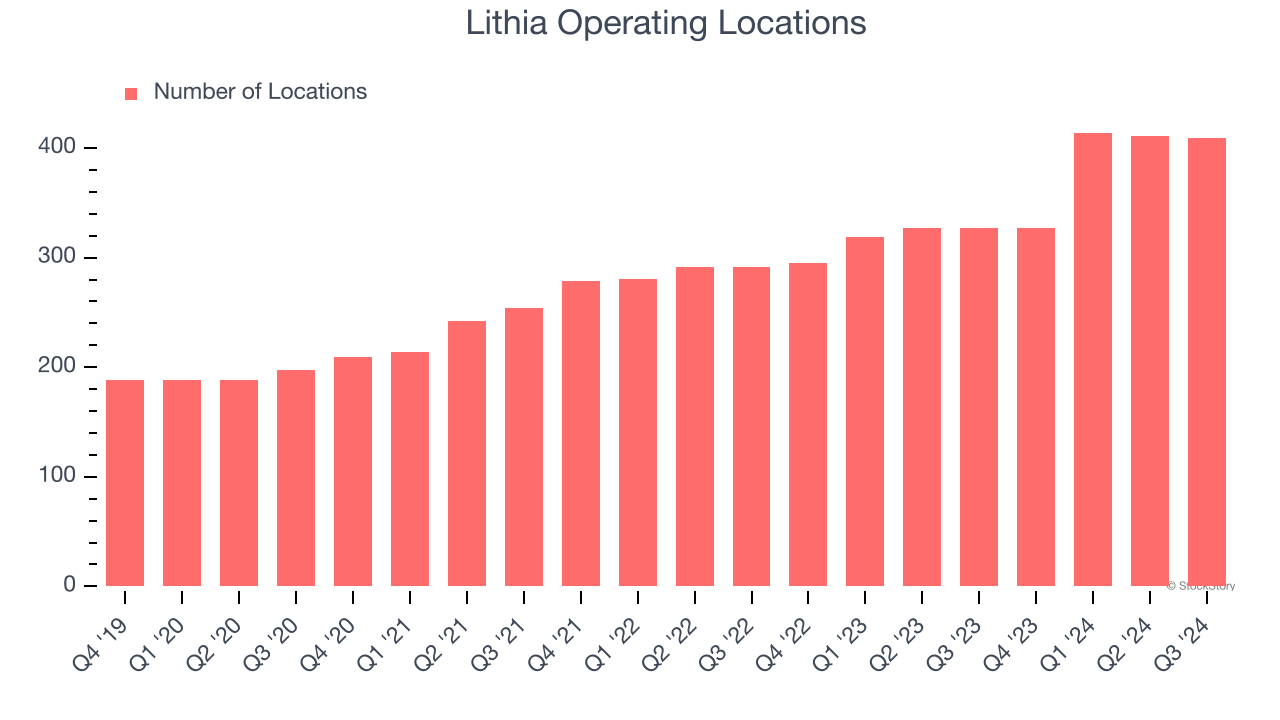

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Over the last two years, Lithia opened new stores at a rapid clip by averaging 18.5% annual growth, among the fastest in the consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Note that Lithia reports its store count intermittently, so some data points are missing in the chart below.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Lithia’s demand has been shrinking over the last two years as its same-store sales have averaged 2.8% annual declines. This performance is concerning - it shows Lithia artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, Lithia’s same-store sales rose 3.1% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

Key Takeaways from Lithia’s Q4 Results

We enjoyed seeing Lithia exceed analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the other hand, its gross margin missed. Overall, this quarter had some key positives. The stock traded up 6.6% to $393 immediately after reporting.

Lithia had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.