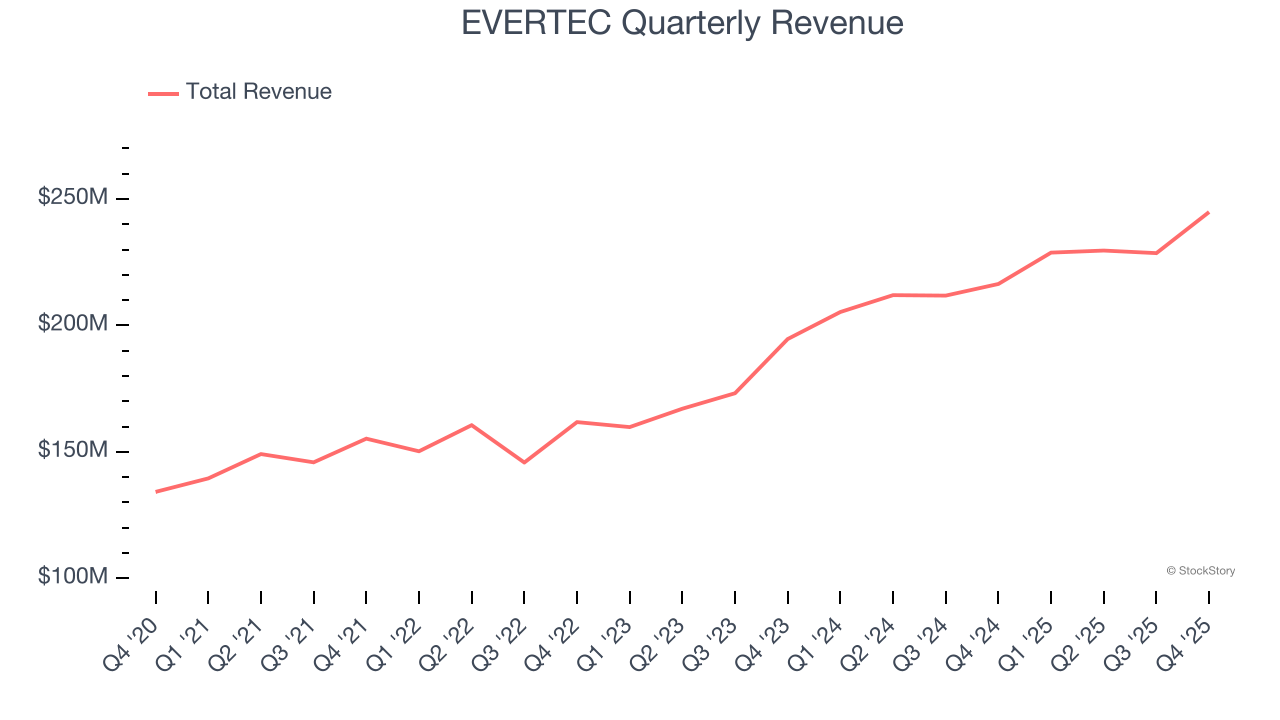

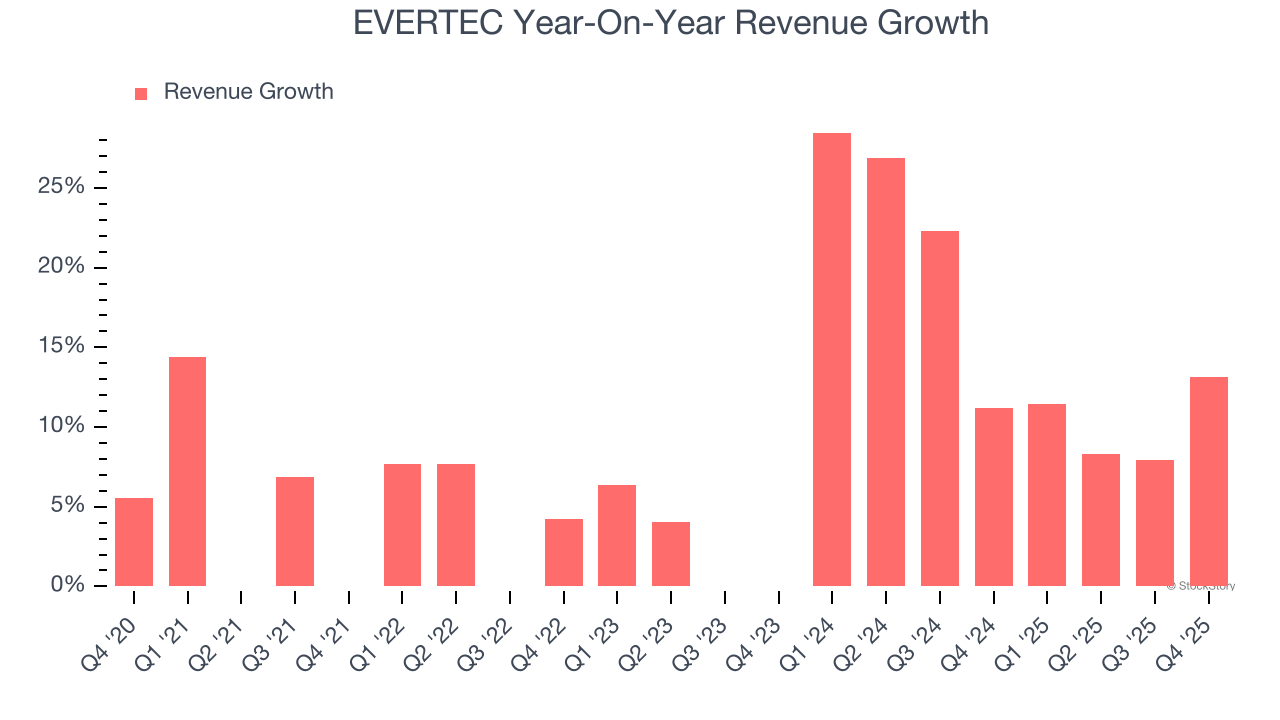

Payment processing company EVERTEC (NYSE: EVTC) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 13.1% year on year to $244.8 million. The company’s full-year revenue guidance of $1.03 billion at the midpoint came in 5.5% above analysts’ estimates. Its non-GAAP profit of $0.93 per share was 2.8% above analysts’ consensus estimates.

Is now the time to buy EVERTEC? Find out by accessing our full research report, it’s free.

EVERTEC (EVTC) Q4 CY2025 Highlights:

- Revenue: $244.8 million vs analyst estimates of $237 million (13.1% year-on-year growth, 3.3% beat)

- Pre-tax Profit: $38.68 million (15.8% margin)

- Adjusted EPS: $0.93 vs analyst estimates of $0.90 (2.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $3.90 at the midpoint, beating analyst estimates by 4%

- Market Capitalization: $1.62 billion

Company Overview

Operating one of Latin America's leading PIN debit networks called ATH, EVERTEC (NYSE: EVTC) is a payment transaction processor and financial technology provider that enables merchants and financial institutions across Latin America and the Caribbean to accept and process electronic payments.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, EVERTEC grew its revenue at a solid 12.8% compounded annual growth rate. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. EVERTEC’s annualized revenue growth of 15.8% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, EVERTEC reported year-on-year revenue growth of 13.1%, and its $244.8 million of revenue exceeded Wall Street’s estimates by 3.3%.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Key Takeaways from EVERTEC’s Q4 Results

We were impressed by EVERTEC’s optimistic full-year revenue guidance, which blew past analysts’ expectations. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 2.4% to $26.39 immediately following the results.

EVERTEC put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).