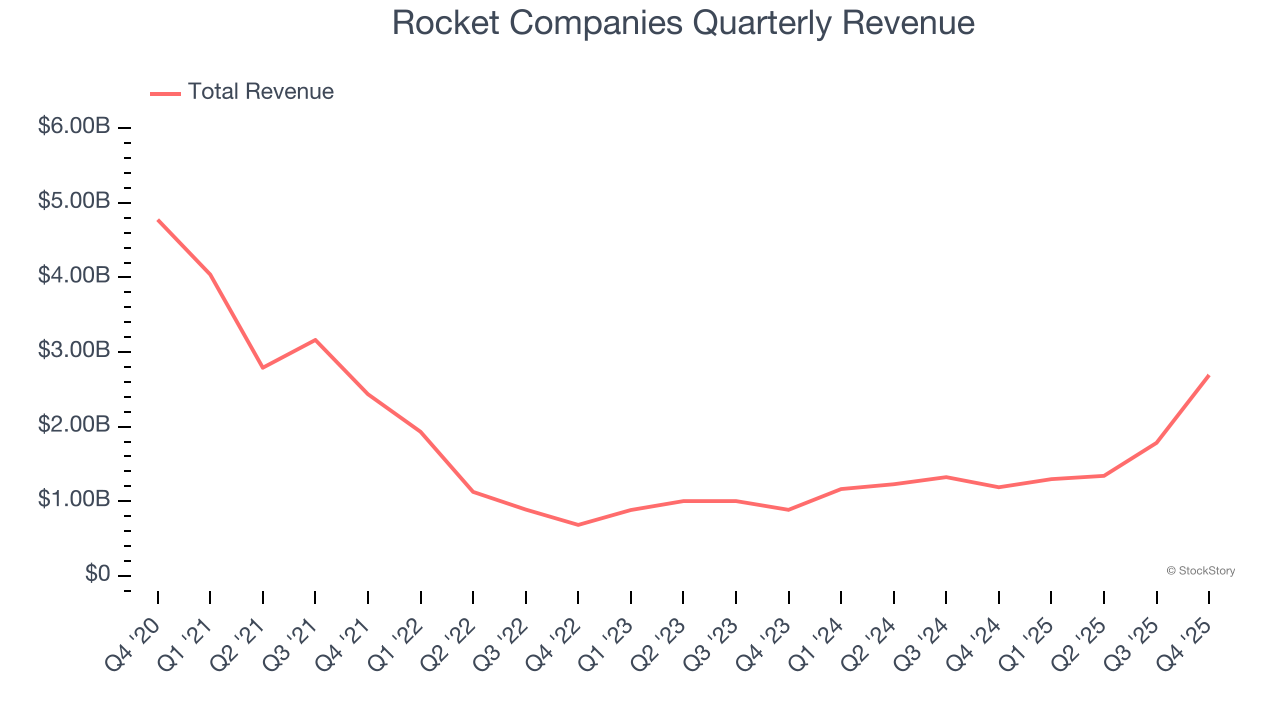

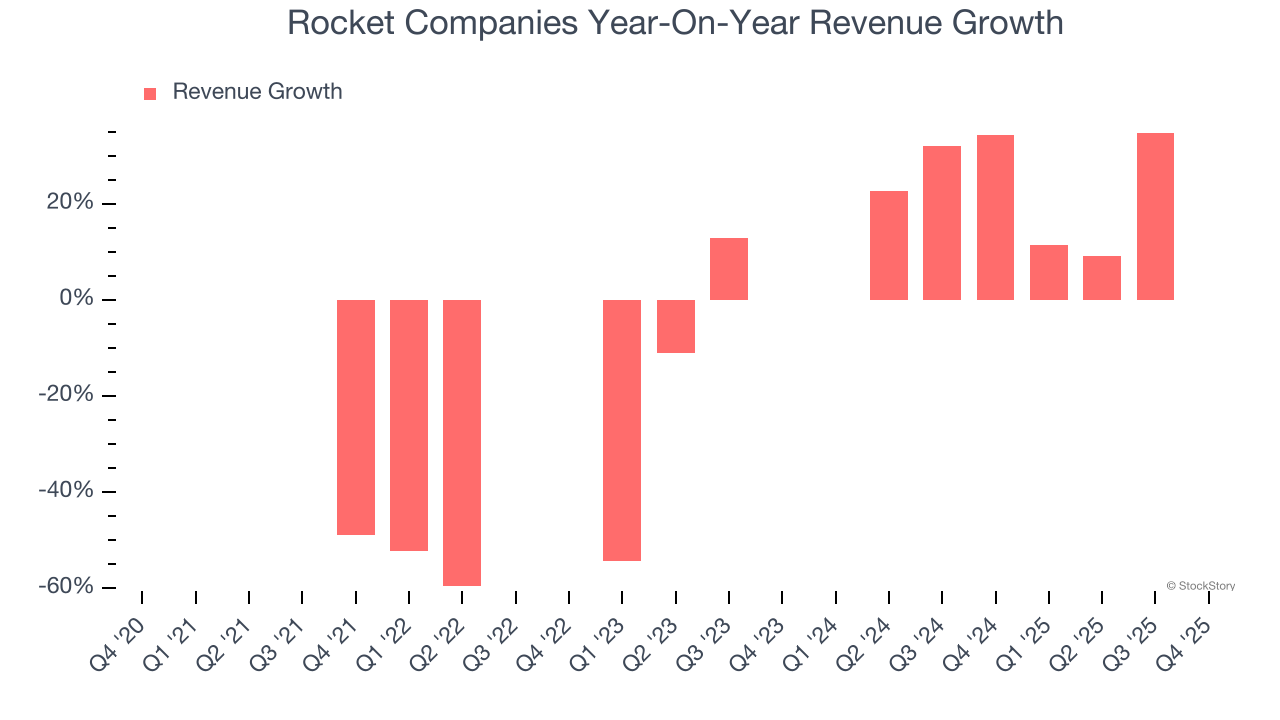

Fintech mortgage provider Rocket Companies (NYSE: RKT) announced better-than-expected revenue in Q4 CY2025, with sales up 127% year on year to $2.69 billion. On top of that, next quarter’s revenue guidance ($2.7 billion at the midpoint) was surprisingly good and 15.9% above what analysts were expecting. Its non-GAAP profit of $0.11 per share was 26.7% above analysts’ consensus estimates.

Is now the time to buy Rocket Companies? Find out by accessing our full research report, it’s free.

Rocket Companies (RKT) Q4 CY2025 Highlights:

- Net Interest Income: $29 million vs analyst estimates of $36.54 million

- Revenue: $2.69 billion vs analyst estimates of $2.21 billion (127% year-on-year growth, 21.7% beat)

- Adjusted EPS: $0.11 vs analyst estimates of $0.09 (26.7% beat)

- Revenue Guidance for Q1 CY2026 is $2.7 billion at the midpoint, above analyst estimates of $2.33 billion

- Market Capitalization: $48.8 billion

"Rocket proved itself this quarter as a category of one. This is the power of an integrated homeownership ecosystem - massive top of funnel, scaled origination-servicing recapture, expansive distribution for industry professionals and a technologically advanced foundation for infinite capacity - built for the AI era," said Varun Krishna, CEO and Director of Rocket Companies.

Company Overview

Born in Detroit during the 1980s and evolving into a tech-driven financial powerhouse, Rocket Companies (NYSE: RKT) is a fintech company that provides digital mortgage lending, real estate services, and personal finance solutions through its technology platform.

Sales Growth

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Rocket Companies’s demand was weak over the last five years as its revenue fell at a 15.9% annual rate. This wasn’t a great result, but there are still things to like about Rocket Companies.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Rocket Companies’s annualized revenue growth of 37.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Rocket Companies reported magnificent year-on-year revenue growth of 127%, and its $2.69 billion of revenue beat Wall Street’s estimates by 21.7%. Company management is currently guiding for a 108% year-on-year increase in sales next quarter.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Key Takeaways from Rocket Companies’s Q4 Results

It was good to see Rocket Companies beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its net interest income missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 9.1% to $19.21 immediately following the results.

Indeed, Rocket Companies had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).