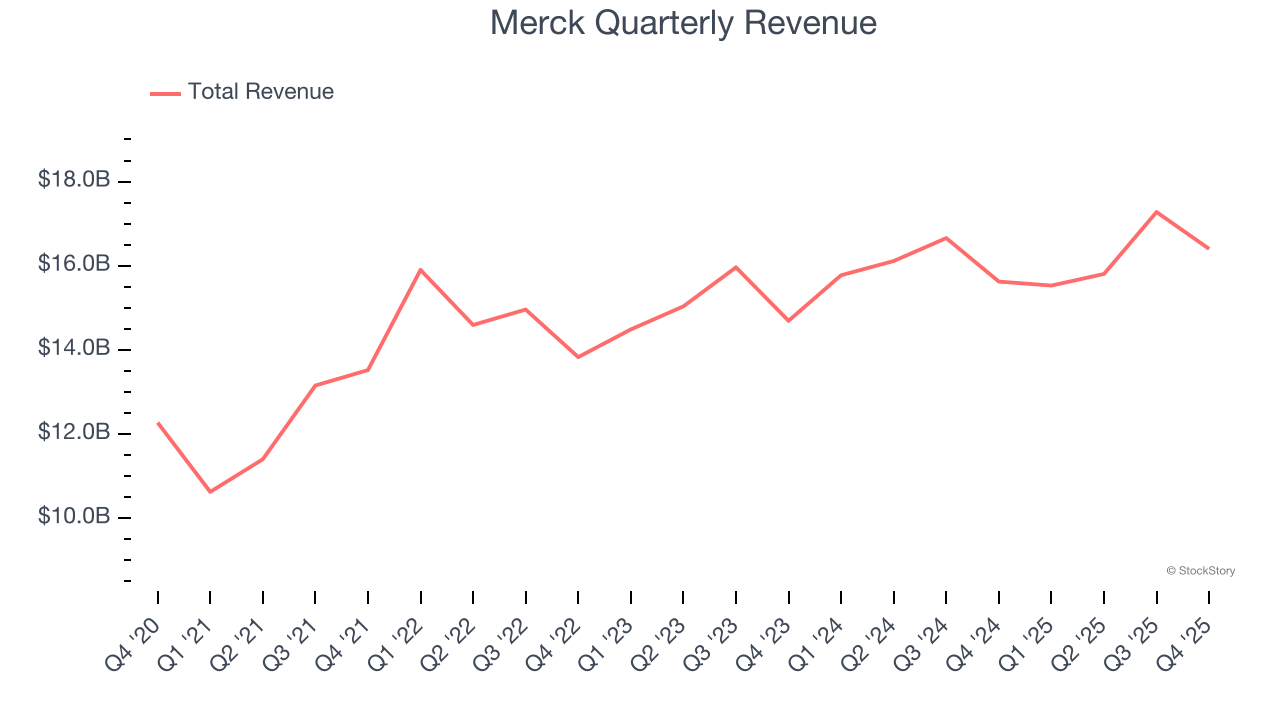

Global pharmaceutical company Merck (NYSE: MRK) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 5% year on year to $16.4 billion. On the other hand, the company’s full-year revenue guidance of $66.25 billion at the midpoint came in 2% below analysts’ estimates. Its non-GAAP profit of $2.04 per share was 1.5% above analysts’ consensus estimates.

Is now the time to buy Merck? Find out by accessing our full research report, it’s free.

Merck (MRK) Q4 CY2025 Highlights:

- Revenue: $16.4 billion vs analyst estimates of $16.12 billion (5% year-on-year growth, 1.8% beat)

- Adjusted EPS: $2.04 vs analyst estimates of $2.01 (1.5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.08 at the midpoint, missing analyst estimates by 9.8%

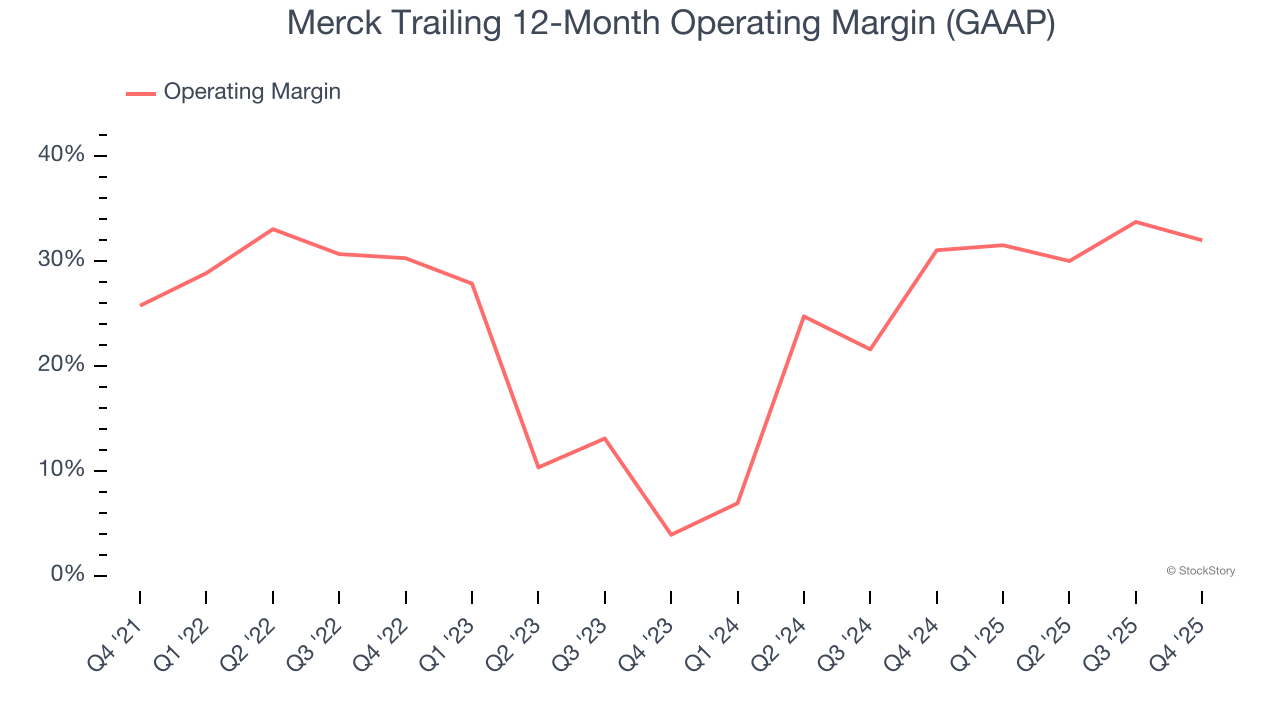

- Operating Margin: 20.9%, down from 27.5% in the same quarter last year

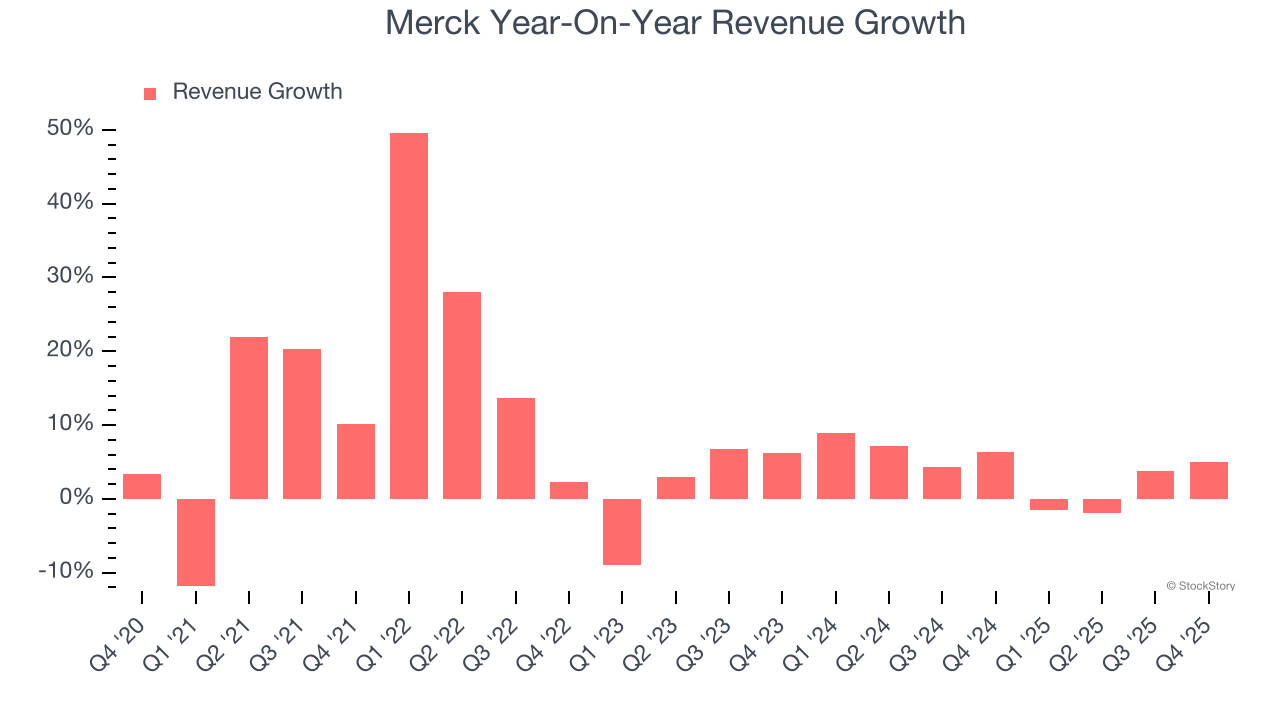

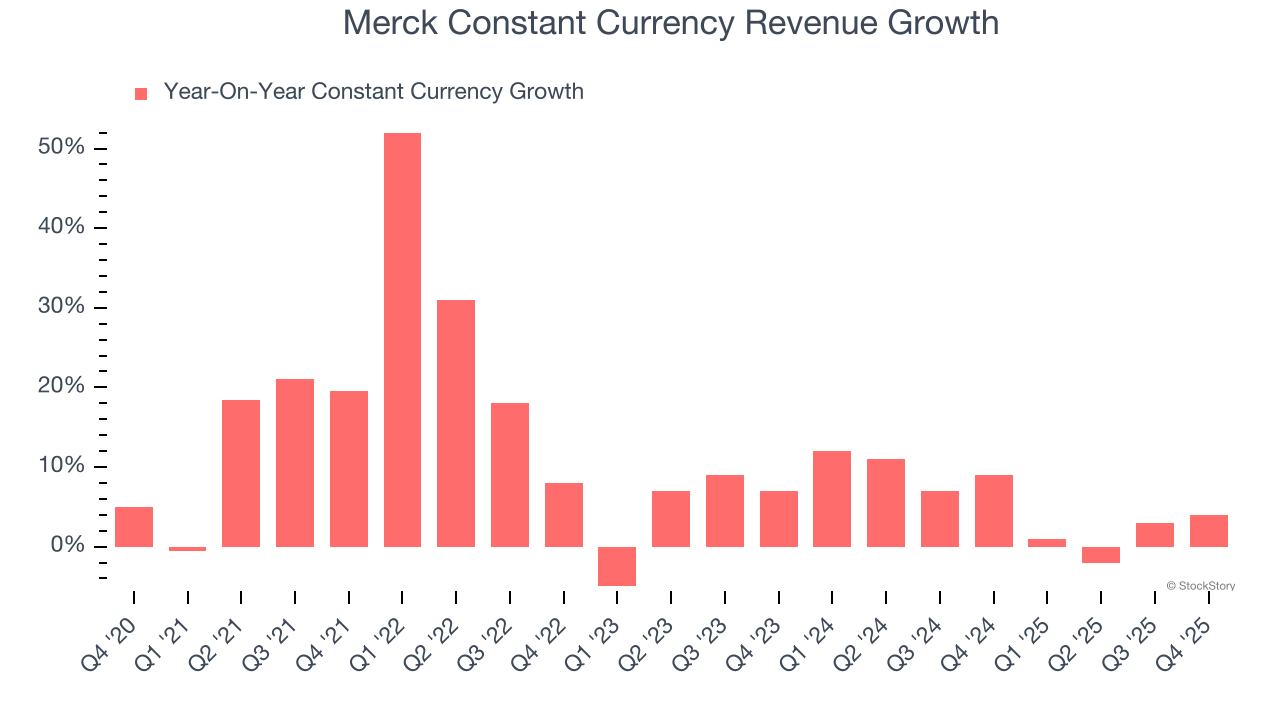

- Constant Currency Revenue rose 4% year on year (9% in the same quarter last year)

- Market Capitalization: $281.4 billion

"In 2025, we continued to advance leading-edge science to deliver transformative medicines and vaccines that are improving health outcomes for patients around the world,” said Robert M. Davis, chairman and chief executive officer.

Company Overview

With roots dating back to 1891 and a portfolio that includes the blockbuster cancer immunotherapy Keytruda, Merck (NYSE: MRK) develops and sells prescription medicines, vaccines, and animal health products across oncology, infectious diseases, cardiovascular, and other therapeutic areas.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Merck’s 7.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Merck’s recent performance shows its demand has slowed as its annualized revenue growth of 3.9% over the last two years was below its five-year trend.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 5.6% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Merck.

This quarter, Merck reported modest year-on-year revenue growth of 5% but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Merck has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 24.7%.

Analyzing the trend in its profitability, Merck’s operating margin rose by 6.2 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 28.1 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Merck generated an operating margin profit margin of 20.9%, down 6.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

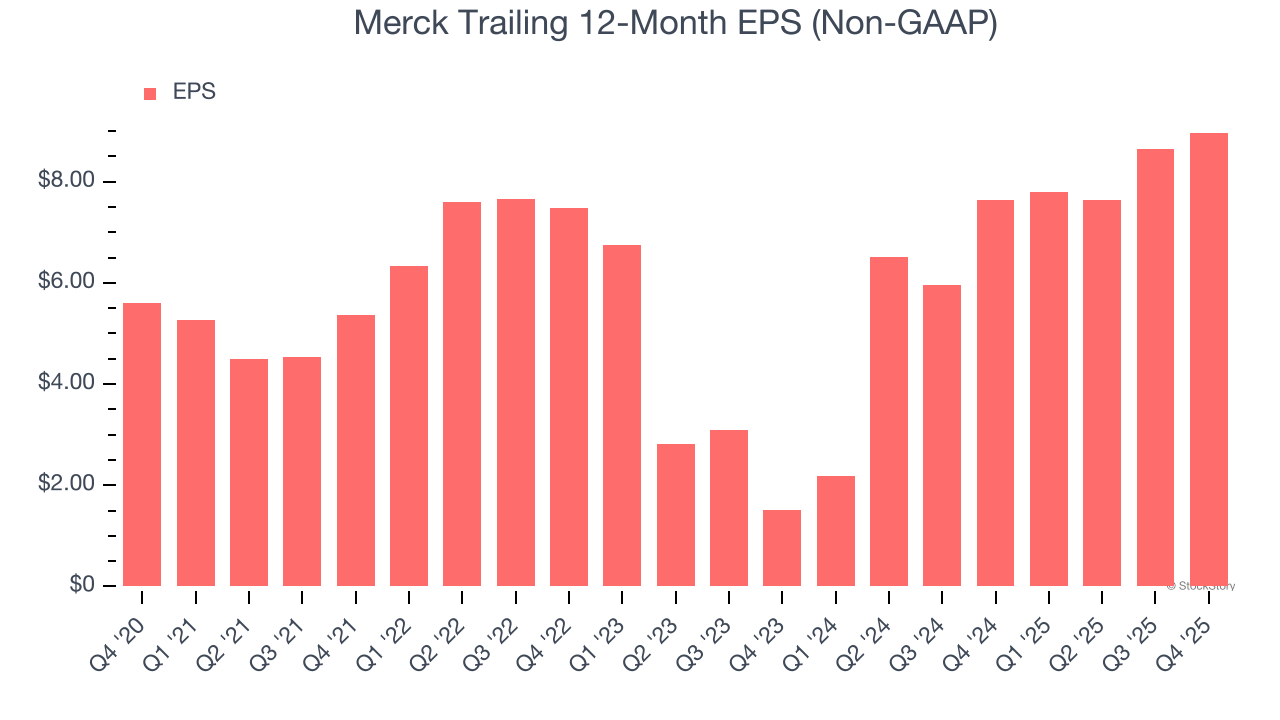

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Merck’s EPS grew at a remarkable 9.9% compounded annual growth rate over the last five years, higher than its 7.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

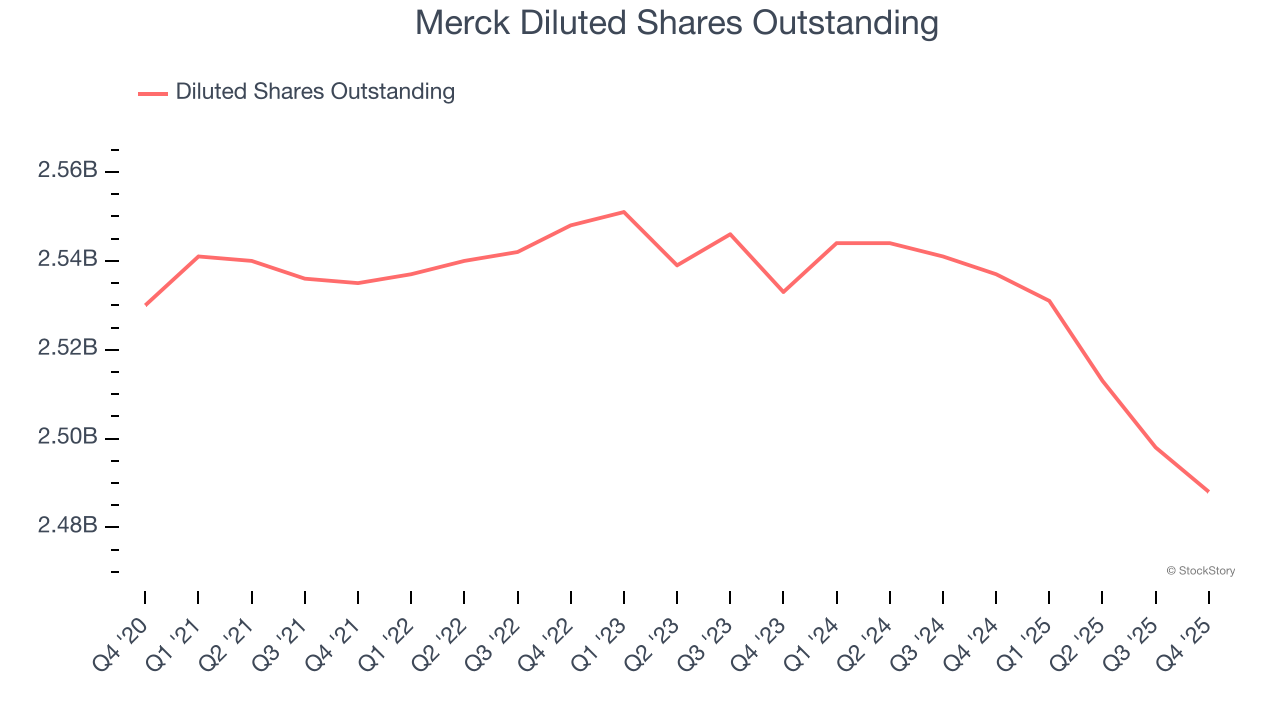

We can take a deeper look into Merck’s earnings to better understand the drivers of its performance. As we mentioned earlier, Merck’s operating margin declined this quarter but expanded by 6.2 percentage points over the last five years. Its share count also shrank by 1.7%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Merck reported adjusted EPS of $2.04, up from $1.72 in the same quarter last year. This print beat analysts’ estimates by 1.5%. Over the next 12 months, Wall Street expects Merck’s full-year EPS of $8.97 to shrink by 40.6%.

Key Takeaways from Merck’s Q4 Results

It was encouraging to see Merck beat analysts’ revenue expectations this quarter. We were also happy its constant currency revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2% to $111.05 immediately following the results.

Merck underperformed this quarter, but does that create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).