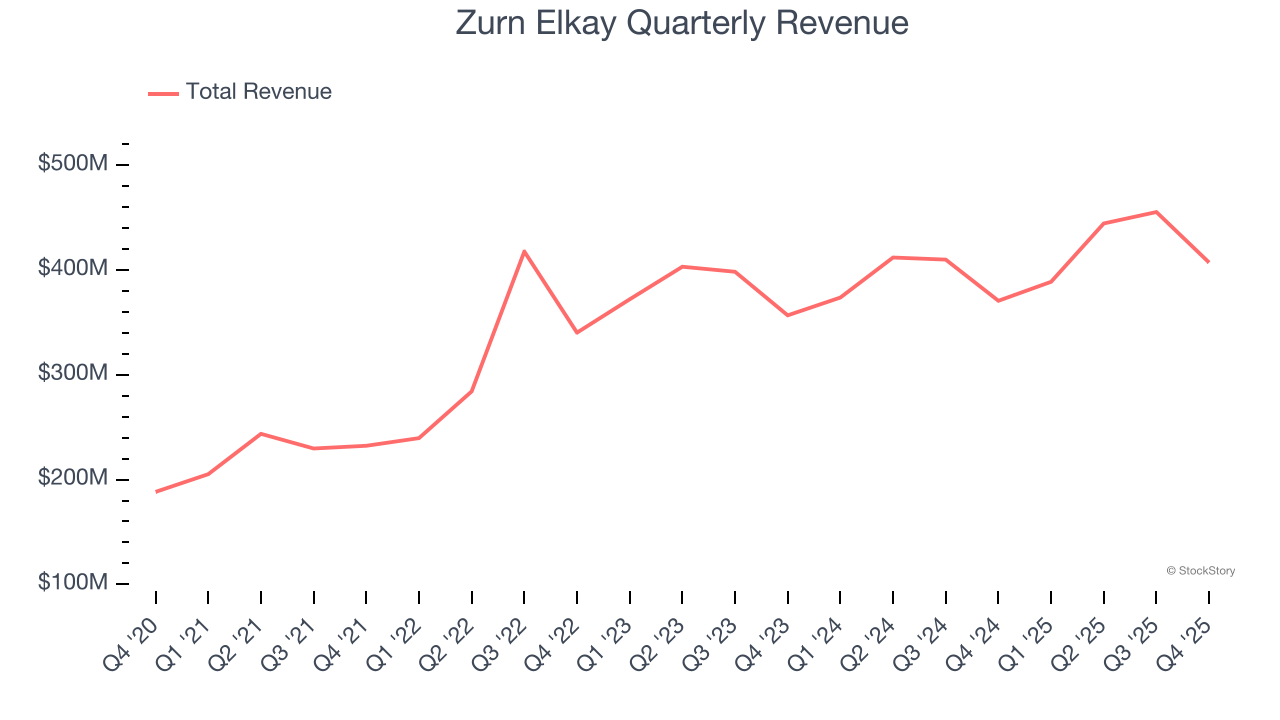

Water management solutions company Zurn Elkay (NYSE: ZWS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 9.8% year on year to $407.2 million. Its non-GAAP profit of $0.36 per share was 5.9% above analysts’ consensus estimates.

Is now the time to buy Zurn Elkay? Find out by accessing our full research report, it’s free.

Zurn Elkay (ZWS) Q4 CY2025 Highlights:

- Revenue: $407.2 million vs analyst estimates of $401.5 million (9.8% year-on-year growth, 1.4% beat)

- Adjusted EPS: $0.36 vs analyst estimates of $0.34 (5.9% beat)

- Adjusted EBITDA: $104.1 million vs analyst estimates of $101.1 million (25.6% margin, 2.9% beat)

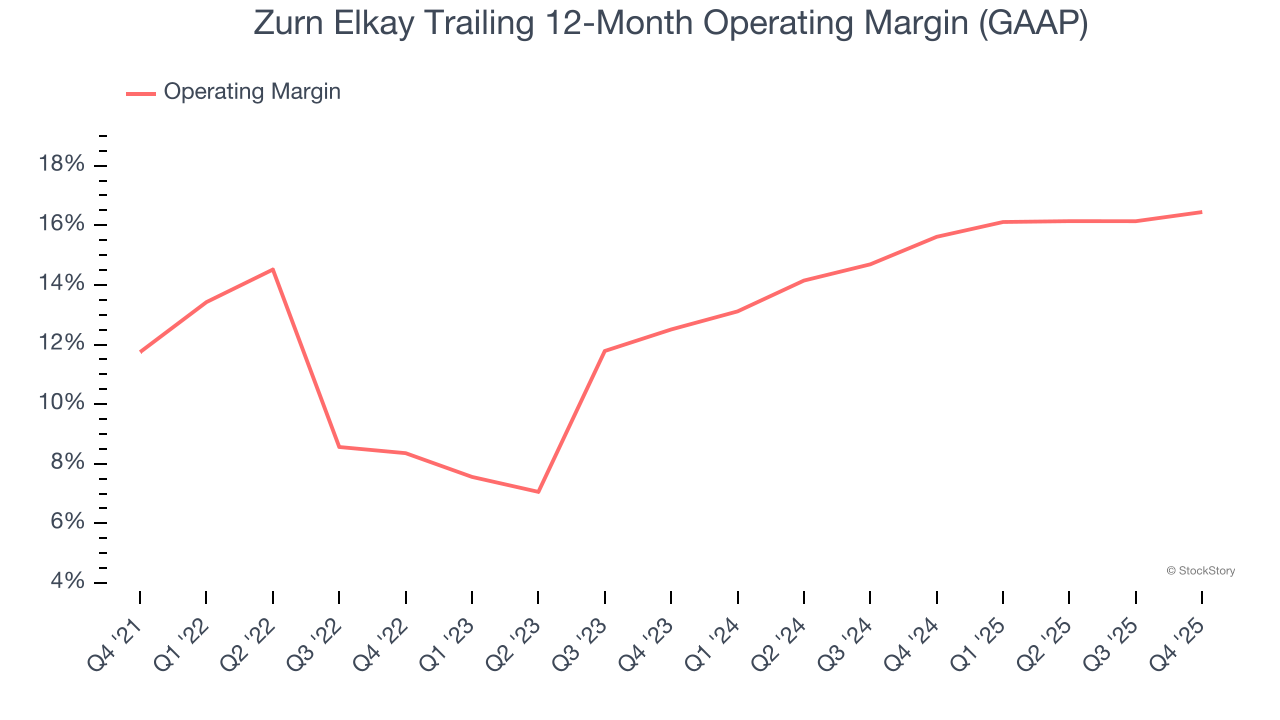

- Operating Margin: 14.8%, up from 13.3% in the same quarter last year

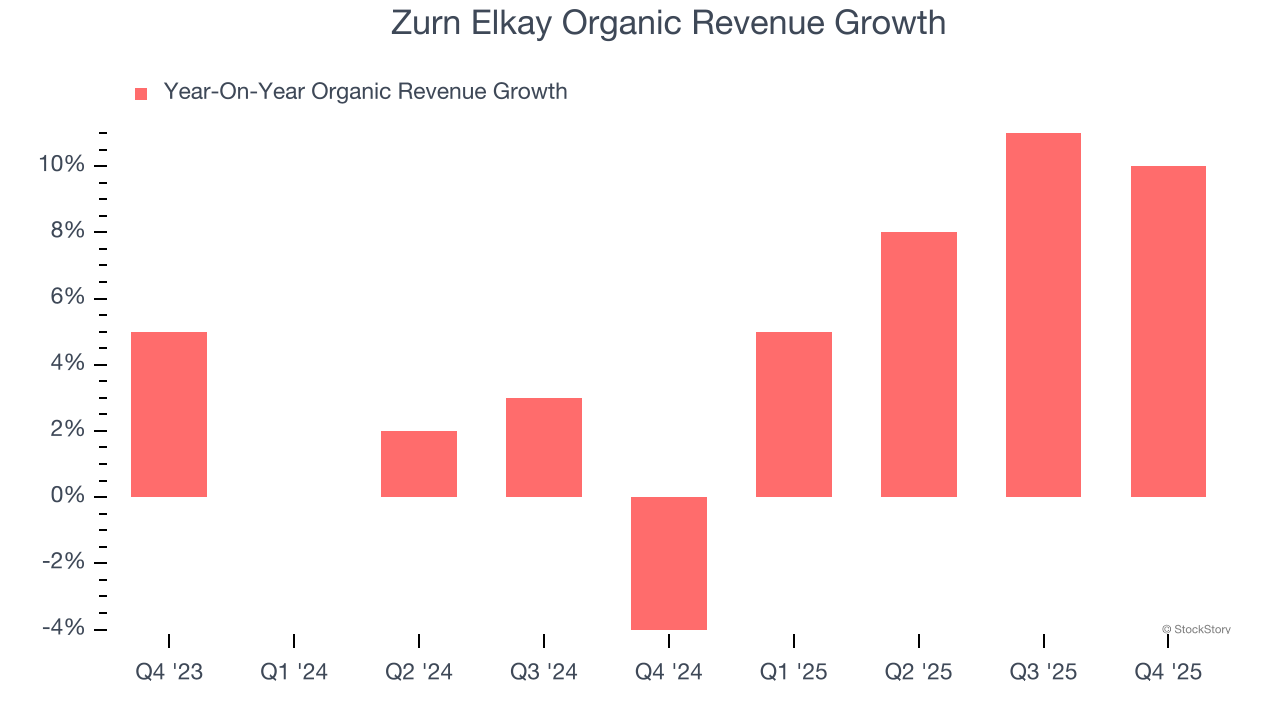

- Organic Revenue rose 10% year on year

- Market Capitalization: $7.85 billion

Todd A. Adams, Chairman and Chief Executive Officer, commented, “We finished 2025 with record annual sales, adjusted EBITDA(1) and free cash flow(1) while repurchasing $160 million of our common stock and increasing our quarterly dividend 22% year over year. We leveraged the Zurn Elkay Business System to drive 8% year-over-year core sales(1) growth and full year adjusted EBITDA(1) of $442 million with margins expanding 120 basis points year over year to 26.1%. Our record free cash flow(1) of $317 million led to net debt leverage(1) of 0.4x at December 31, 2025. We exit 2025 with a balance sheet, outlook and management capacity that gives us the ability to deploy capital to continue to deliver shareholder value.”

Company Overview

Claiming to have saved more than 30 billion gallons of water, Zurn Elkay (NYSE: ZWS) provides water management solutions to various industries.

Revenue Growth

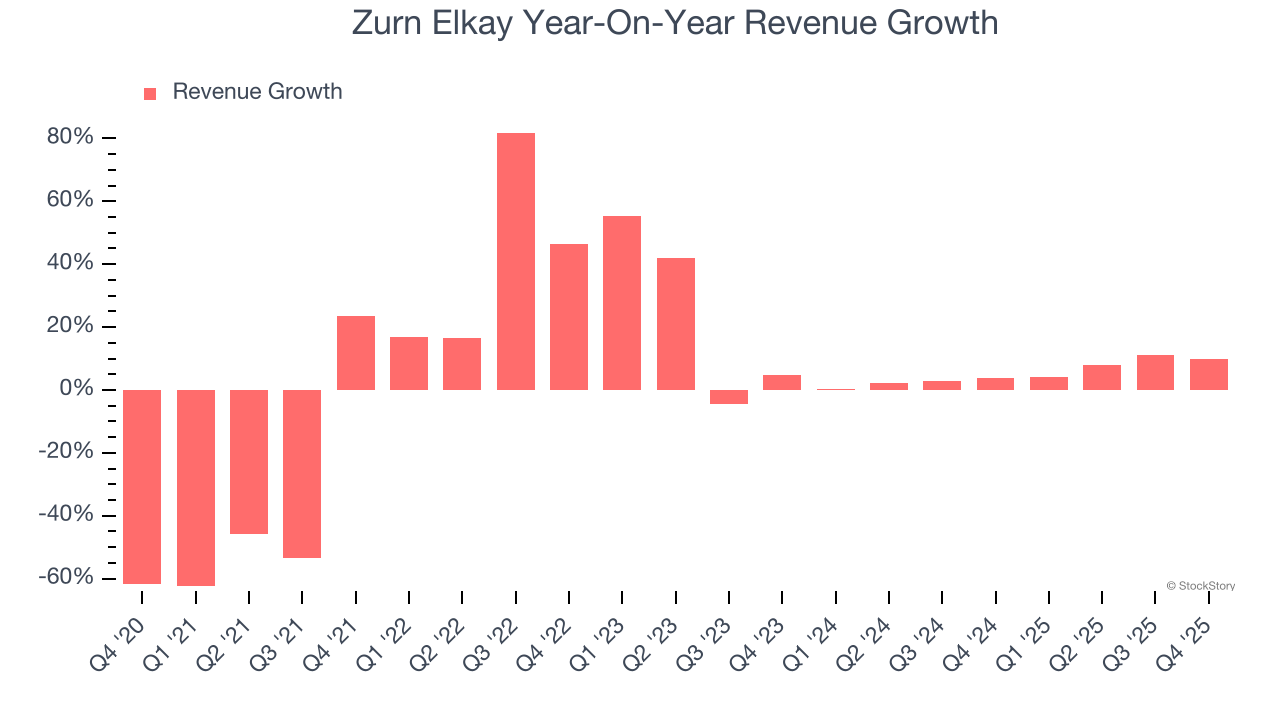

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Zurn Elkay struggled to consistently increase demand as its $1.70 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of lacking business quality.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Zurn Elkay’s annualized revenue growth of 5.3% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Zurn Elkay’s organic revenue averaged 4.4% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Zurn Elkay reported year-on-year revenue growth of 9.8%, and its $407.2 million of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not accelerate its top-line performance yet.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Zurn Elkay has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 13.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Zurn Elkay’s operating margin rose by 4.7 percentage points over the last five years, showing its efficiency has improved.

In Q4, Zurn Elkay generated an operating margin profit margin of 14.8%, up 1.5 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

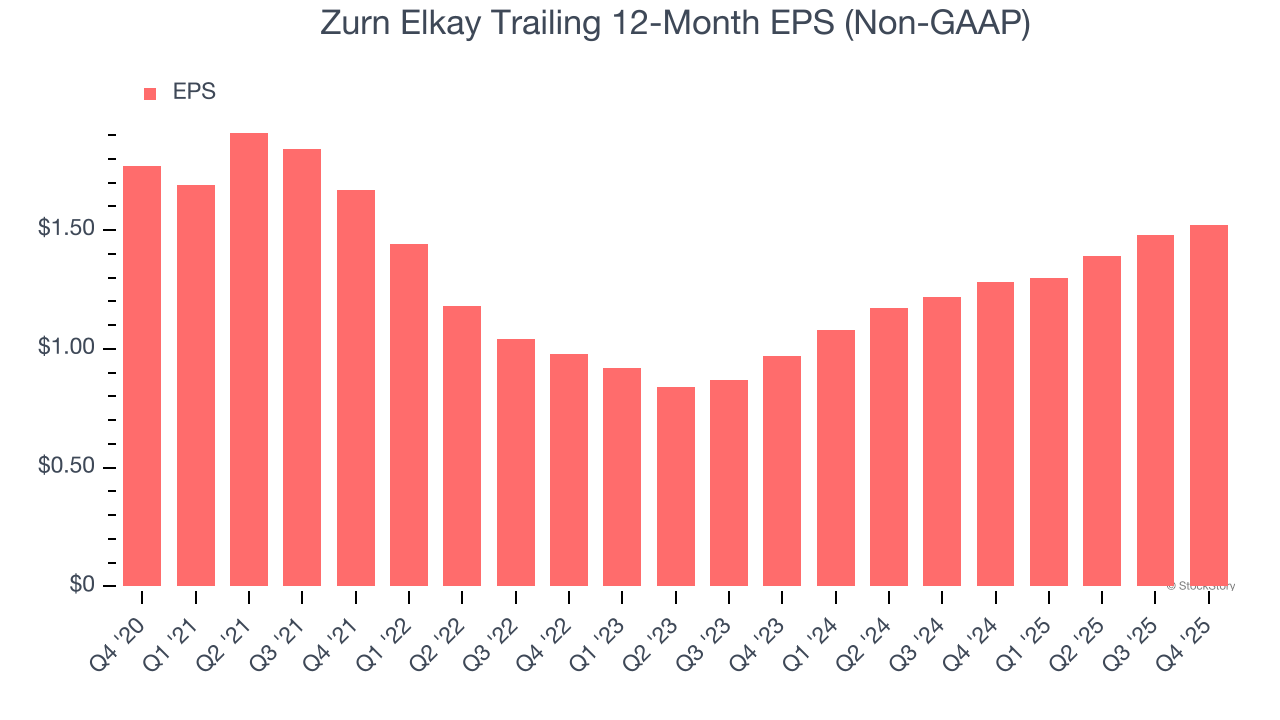

Sadly for Zurn Elkay, its EPS declined by 3% annually over the last five years while its revenue was flat. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

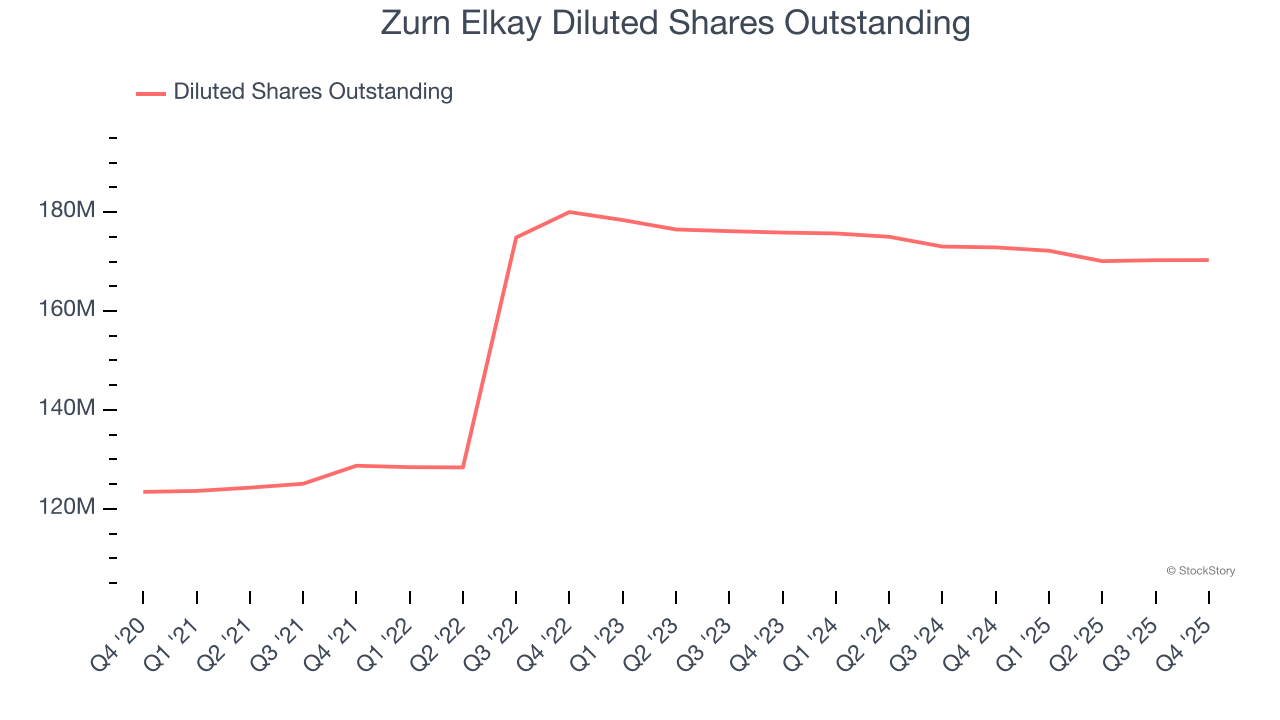

Diving into the nuances of Zurn Elkay’s earnings can give us a better understanding of its performance. A five-year view shows Zurn Elkay has diluted its shareholders, growing its share count by 38%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Zurn Elkay, its two-year annual EPS growth of 25.2% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Zurn Elkay reported adjusted EPS of $0.36, up from $0.32 in the same quarter last year. This print beat analysts’ estimates by 5.9%. Over the next 12 months, Wall Street expects Zurn Elkay’s full-year EPS of $1.52 to grow 8.5%.

Key Takeaways from Zurn Elkay’s Q4 Results

It was good to see Zurn Elkay narrowly top analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $47 immediately after reporting.

So should you invest in Zurn Elkay right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).