We maintain several market timing models, each with differing time horizons. The "Ultimate Market Timing Model" is a long-term market timing model based on the research outlined in our post, Building the ultimate market timing model. This model tends to generate only a handful of signals each decade.

The Trend Model is an asset allocation model which applies trend following principles based on the inputs of global stock and commodity price. This model has a shorter time horizon and tends to turn over about 4-6 times a year. In essence, it seeks to answer the question, "Is the trend in the global economy expansion (bullish) or contraction (bearish)?"

My inner trader uses a trading model, which is a blend of price momentum (is the Trend Model becoming more bullish, or bearish?) and overbought/oversold extremes (don't buy if the trend is overbought, and vice versa). Subscribers receive real-time alerts of model changes, and a hypothetical trading record of the those email alerts are updated weekly here. The hypothetical trading record of the trading model of the real-time alerts that began in March 2016 is shown below.

The latest signals of each model are as follows:

- Ultimate market timing model: Buy equities*

- Trend Model signal: Bearish*

- Trading model: Bearish*

Update schedule: I generally update model readings on my site on weekends and tweet mid-week observations at @humblestudent. Subscribers receive real-time alerts of trading model changes, and a hypothetical trading record of the those email alerts is shown here.

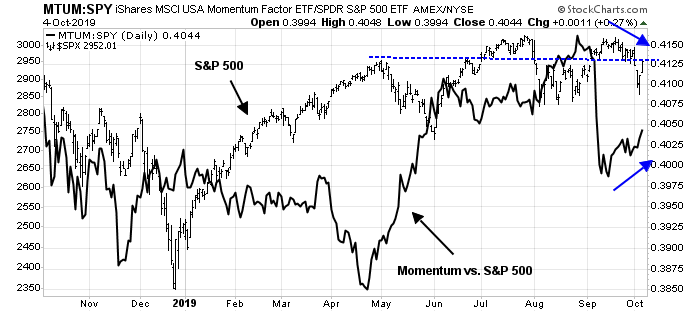

An update on the Momentum Massacre

Remember the Momentum Massacre? Too many investors were in a crowded short in the stock market. The cautiousness was manifesting itself in the price momentum factor, which was showing up in low volatility, low beta, defensive, and value stocks. The crowded short and long momentum trade began to unwind in late August, and accelerated when the SPX staged an upside breakout from its trading range at 2960 in early September.

The reversal was dramatic enough that JPM quant Marko Kolanovic called it a "once in a decade trade" (per CNBC). He made the case that both hedge fund and institutional positioning was too cautious, and a short-covering rally would spark a stampede by the slow moving but big money institutional behemoths to buy beta. Moreover, the reversal could also be a signal for a long awaited turn from growth to value investing.

Since then, returns to the price momentum factor has stabilized and begun to turn up again. It is time for an update.

More importantly, our analysis of the returns to differing factors and sectors is revealing of likely future market direction.

The full post can be found here.