Despite a modest pullback over the past few weeks, Arista Networks (ANET) remains one of Wall Street’s most compelling growth stories, and one prominent analyst believes there’s still significant upside ahead.

Evercore ISI’s Amit Daryanani recently lifted the firm’s price target on Arista to $200, marking the street high and signaling confidence in the company’s expanding role in artificial intelligence (AI)-driven data centers and hyperscale networking infrastructure. At current levels, that target implies over 50% upside over the coming year, underpinned by robust earnings beats, and sustained demand for cloud-scale switching and routing solutions.

With enterprise and AI workloads continuing to surge globally, Arista’s blend of solid fundamentals and industry tailwinds should allow it to achieve the ambitious price target. What should be your move? Let’s discuss.

About Arista Networks Stock

Arista Networks is a leading computer networking company that develops, markets, and sells high-performance, data-driven networking solutions for cloud and enterprise environments, including data centers, campus networks, and AI infrastructure. Headquartered in Santa Clara, California, the company’s products, anchored by its proprietary Extensible Operating System (EOS) and a broad portfolio of Ethernet switches, routers, and software-defined networking platforms, are designed to deliver scalability, automation, analytics, and security for modern network architectures. The company has a market cap of around $167 billion, reflecting its status as a major player in the networking hardware and cloud infrastructure sector.

Arista’s share price has experienced significant volatility over the past year as investors have weighed its leadership in AI-ready networking against macroeconomic headwinds and competitive pressures. Over the trailing 52-week period, the stock reached a high of $164.94 in October 2025, and is currently down by 26.6% from that peak.

Despite pulling back, ANET has still delivered strong absolute returns, up 35.14% over the past year, underscoring the long-term appeal of its growth trajectory in cloud and AI networking.

In 2026, Arista’s stock performance has been more muted. While broader tech markets have rallied on renewed AI optimism, ANET’s share price has only declined marginally year-to-date (YTD) by 0.60%.

Additionally, Arista’s share price has experienced meaningful swings recently, with a notable intraday jump of 3.2% on Feb. 25, amid broader sector tailwinds from the ongoing AI infrastructure arms race, including sentiments around expanded AI hardware agreements such as the multi-year Advanced Micro Devices (AMD) and Meta Platforms (META) deal, which underscored strengthening demand fundamentals for data-center networking, a key end market for Arista.

The stock is currently trading at 40.98 times forward earnings, which is a premium to the sector median.

Steady Financial Performance

Arista Networks released its fourth quarter and full year 2025 results on Feb. 12. For Q4, Arista reported revenue of $2.5 billion, up 28.9% year-over-year (YOY) compared to the fourth quarter of 2024, reflecting sustained demand for high-performance networking solutions across hyperscale cloud, enterprise, and AI segments.

Its non-GAAP net income was around $1.1 billion, up from $849.6 million in Q4 2024, while non-GAAP EPS of $0.82 represented 24.2% YOY growth, topping estimates and signaling improved profitability alongside top-line expansion. Gross margins remained strong, with non-GAAP gross margin at 63.4%, slightly lower than the prior year period but still well above industry norms.

For the full year ended December 31, 2025, Arista delivered revenue of $9 billion, representing 28.6% growth over fiscal 2024, underscoring robust secular demand for its networking platforms in both cloud and AI deployments. Non-GAAP net income reached $3.8 billion, or $2.98 per share, up from nearly $3 billion, or $2.32 per share, in 2024. Arista maintained its full-year GAAP and non-GAAP gross margin levels of 64.1% and 64.6%, respectively.

Furthermore, Arista provided guidance for Q1 2026, expecting revenue of $2.6 billion, with a non-GAAP gross margin targeted in the 62% to 63% range and an operating margin near 46%.

Analysts forecast EPS of $3.14 for fiscal 2026, an 15.9% YOY jump, followed by a further 18.5% rise to $3.72 in 2027.

What Do Analysts Expect for Arista Networks Stock?

Recently, Evercore ISI reiterated its “Outperform” rating and $200 price target on Arista Networks, reflecting confidence in the company’s AI infrastructure momentum.

Also, Piper Sandler raised its price target on Arista Networks to $175 from $159 while reiterating an “Overweight” rating, following better-than-expected quarterly results.

Additionally, Needham raised its price target on Arista Networks to $185 from $165 while maintaining a “Buy” rating, citing the company’s strong Q4 2025 results. Needham views Arista as well-positioned in the “generational investment cycle” due to its ability to capitalize on increasing AI spending.

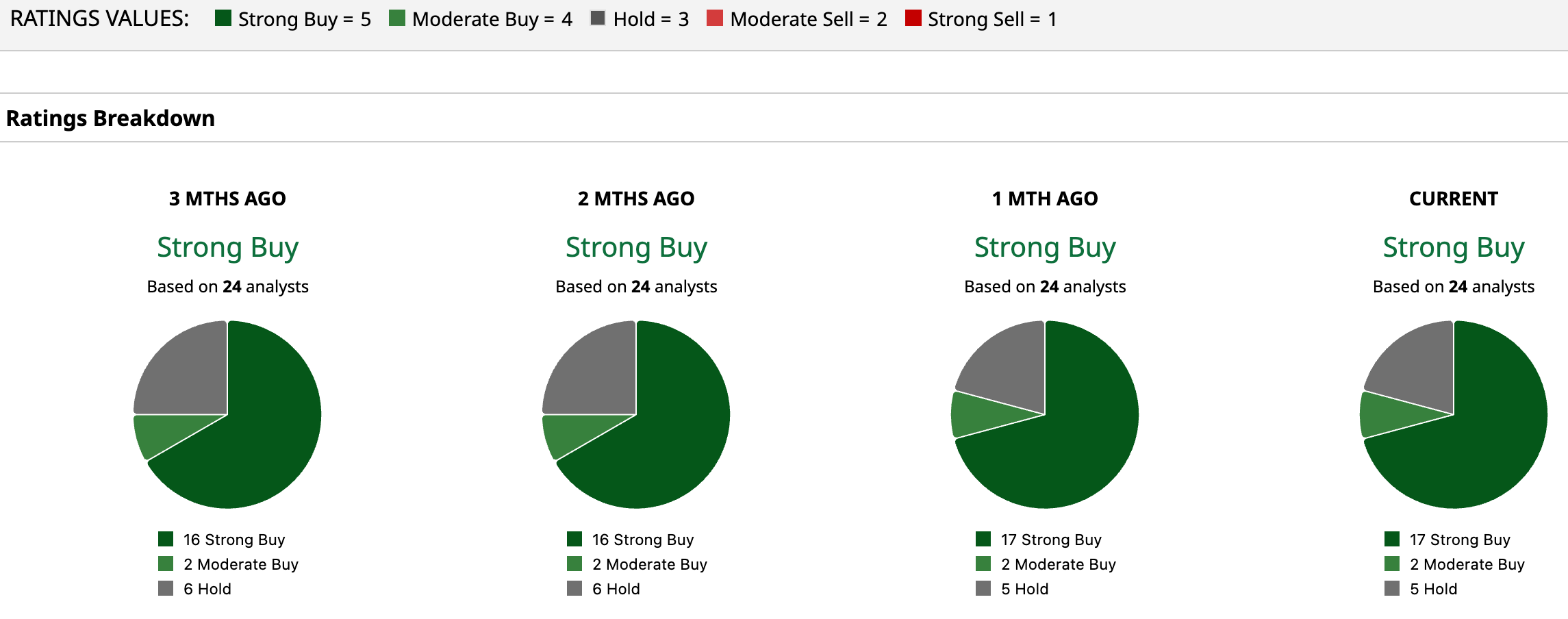

Wall Street is majorly bullish on ANET. Overall, ANET has a consensus “Strong Buy” rating. Of the 24 analysts covering the stock, 17 advise a “Strong Buy,” two suggest a “Moderate Buy,” and the remaining five analysts are on the sidelines, giving it a “Hold” rating.

ANET’s average analyst price target of $179.91 suggests an upside potential of 38.1%, while Evercore’s Street-high target price of $200 suggests that the stock could rally as much as 53.6%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart