In a week that many analysts are calling a "watershed moment" for the future of transportation and artificial intelligence, Tesla (NASDAQ: TSLA) reported fourth-quarter 2025 earnings that defied the grim expectations of the "EV winter." On January 28, 2026, the company posted a non-GAAP earnings per share (EPS) of $0.50, comfortably clearing the $0.45 consensus estimate. However, the financial beat was merely the backdrop for a much more radical announcement: a $2 billion strategic investment into Elon Musk’s artificial intelligence venture, xAI, and a definitive pivot toward a "robotics-first" corporate strategy.

The shift comes at a precarious time for Tesla’s traditional automotive core. Despite the earnings beat, the company confirmed that 2025 marked its first back-to-back annual decline in vehicle deliveries, falling 8.6% year-over-year to 1.63 million units. By prioritizing the development of its "Cybercab" robotaxi and the Optimus humanoid robot over the aging Model S and Model X lines—which are being discontinued—Tesla is effectively signaling that its future no longer depends on selling cars to humans, but on the deployment of autonomous intelligence.

Financial Resilience Amidst an Industry Contraction

The fourth-quarter results revealed a company that has become adept at protecting its bottom line even as its market dominance in the electric vehicle sector erodes. While total revenue dipped 3% to $24.9 billion, Tesla (NASDAQ: TSLA) managed a surprise recovery in automotive gross margins, which climbed to 20.1%—beating the 17.1% forecasted by Wall Street. This margin expansion was largely attributed to a massive cost-cutting initiative and the maturation of production efficiencies at Giga Berlin and Giga Texas. The revenue shortfall in the automotive segment was partially cushioned by record-breaking growth in the Tesla Energy division, which has become a vital pillar of the company’s profitability.

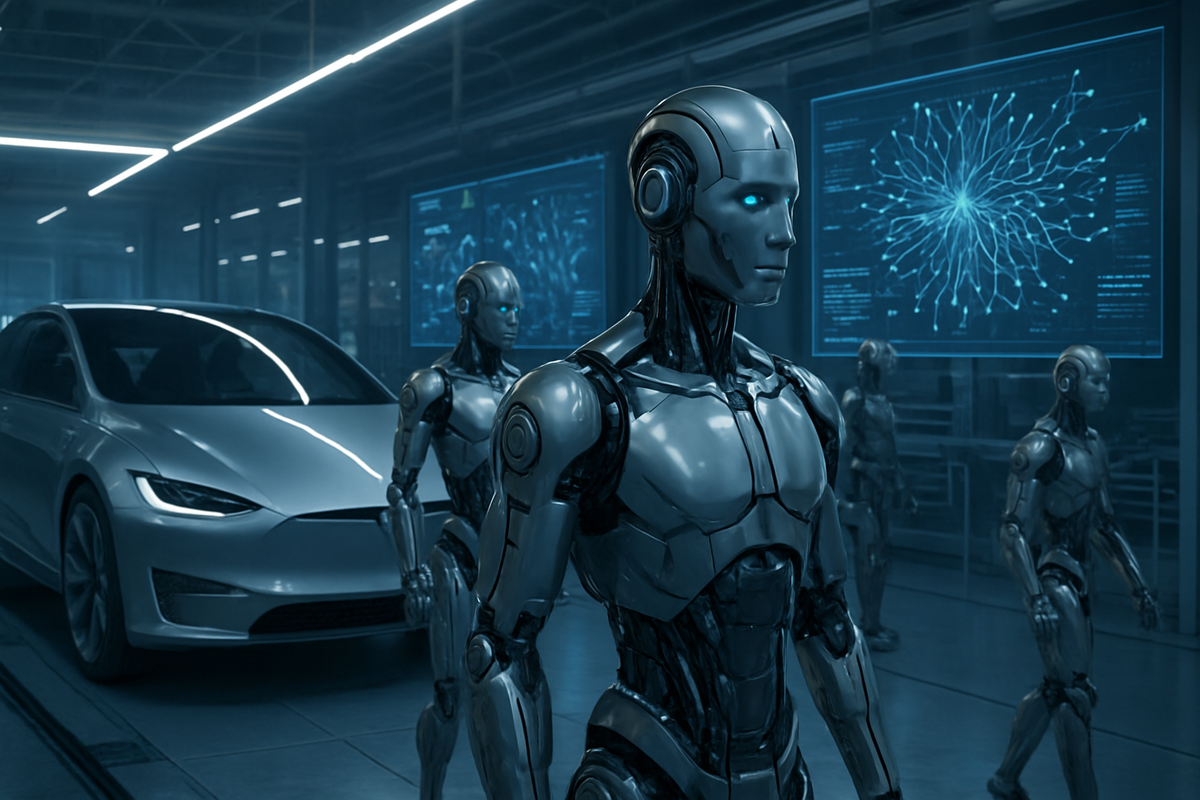

The most controversial element of the report was the confirmed $2 billion investment in xAI. Tesla acquired Series E preferred shares in the startup at a staggering $230 billion valuation. This move follows months of speculation regarding how Musk would integrate his disparate ventures. The investment is framed as a key component of "Master Plan Part IV," intended to provide Tesla with a direct pipeline to xAI’s "Grok" large language models. This integration aims to bridge the gap between digital AI and "Physical AI," allowing Tesla’s FSD (Full Self-Driving) and Optimus systems to process complex real-world reasoning more effectively than traditional neural networks.

Initial market reactions were a microcosm of the current investor divide regarding Tesla. In the hours following the announcement, shares surged over 4% as "AI bulls" cheered the formalization of the xAI partnership and the concrete timeline for the Cybercab. However, by the close of the week on January 30, 2026, those gains had tempered. Skeptics pointed to the massive capital expenditure (CapEx) forecast, which is expected to double to over $20 billion in 2026, as the company retools its factories for humanoid robot production and autonomous taxi fleets.

Market Shift: Identifying the New Winners and Losers

As Tesla reorients itself, the landscape of the global electric vehicle market is being fundamentally reshaped. The primary beneficiary of Tesla’s cooling automotive growth has been BYD (OTC:BYDDF), which officially claimed the title of the world’s top BEV seller in 2025 with over 2.25 million deliveries. BYD’s ability to dominate the mass market while Tesla focuses on high-margin robotics has solidified the Chinese automaker’s position as the global volume leader. Similarly, tech giant Xiaomi (OTC:XIACF) has emerged as a major winner; its SU7 sedan reportedly outsold the Tesla Model 3 in the Chinese premium segment throughout 2025, proving that consumer electronics expertise can translate successfully into the automotive space.

Conversely, the "losers" in this pivot appear to be the traditional luxury EV brands and the legacy automotive players who are still struggling to achieve profitability in their electric segments. With Tesla (NASDAQ: TSLA) discontinuing the Model S and Model X, there is a vacuum in the premium EV market, but it is one that Tesla seems happy to surrender in exchange for the "trillion-dollar opportunity" of robotics. Companies like Lucid Group (NASDAQ: LCID) and Rivian (NASDAQ: RIVN) may find temporary breathing room in the luxury niche, but they now face a competitor that is no longer fighting for their customers, but rather for the entire infrastructure of future labor and transit.

Within the robotics sector, the investment in xAI puts pressure on established AI hardware and software firms. While NVIDIA (NASDAQ: NVDA) remains the primary provider of the compute power necessary for these advancements, Tesla’s push for vertical integration—combining its own "Dojo" supercomputer with xAI’s software—represents a long-term threat to the broader AI ecosystem's reliance on standardized platforms.

A High-Stakes Bet on "Physical AI"

Tesla’s transition fits into a broader industry trend where the "first-mover advantage" in EVs has peaked, and the next frontier is autonomous physical agency. This "Physical AI" trend is driven by a global labor shortage and the plummeting cost of automation sensors and actuators. By shifting focus to Optimus, Tesla is attempting to do for the labor market what it did for the gas-powered car market fifteen years ago: make a radical new technology economically viable through massive scale.

The regulatory implications of this shift are profound. As Tesla (NASDAQ: TSLA) moves from being a car manufacturer to a robotics and autonomous transit operator, it enters a regulatory "Wild West." The Cybercab trials in Austin, Texas, which are currently operating without safety monitors, are being watched closely by the National Highway Traffic Safety Administration (NHTSA). Any significant safety incident could derail the April 2026 launch and set a chilling precedent for the entire autonomous vehicle industry.

Historically, this pivot is reminiscent of Apple's shift from being a computer company to a mobile and services company. Just as Apple sacrificed its identity as a PC manufacturer to capture the smartphone era, Musk is sacrificing Tesla’s identity as a car company to capture the robotics era. However, the capital requirements for robotics are exponentially higher than for consumer electronics, making this one of the most expensive corporate gambles in history.

The Road to 2027: What Lies Ahead

In the short term, Tesla (NASDAQ: TSLA) faces a "valley of death" as it transitions production lines. The discontinuation of the Model S and Model X will lead to a temporary revenue gap that must be filled by the Energy division and continued cost-cutting in Model 3 and Model Y production. Investors should expect high volatility as the company begins the grueling process of setting up a 1-million-unit annual production capacity for Optimus in Fremont.

Long-term, the success of the $2 billion xAI investment will be measured by the "intelligence" of the Cybercab. If the integration of Grok-based reasoning allows Tesla to achieve Level 5 autonomy by 2027, the company’s valuation could decouple entirely from the automotive sector and move toward the valuations of the "Magnificent Seven" tech giants. However, if production hurdles for Optimus mirror the "production hell" seen during the Model 3 launch, Tesla may find itself overleveraged and vulnerable.

The most likely scenario is a period of "empire consolidation." Rumors of a potential merger or a more formalized "Musk Galaxy" of companies involving SpaceX, xAI, and Tesla have reached a fever pitch. Such a move would allow Tesla to share the enormous R&D costs of robotics and aerospace-grade AI across a much broader base of private and public capital.

Investor Outlook and Final Assessment

The Q4 2025 earnings report will be remembered as the moment Tesla (NASDAQ: TSLA) officially stopped being a car company. The EPS beat of $0.50 demonstrated that the company is still a disciplined financial engine, but the $2 billion xAI investment and the robotics pivot are the true stories. Tesla is betting that the consumer EV market has reached a saturation point and that the only path to 10x growth lies in replacing human labor and traditional car ownership.

For investors, the coming months will require a focus on "milestone metrics" rather than just delivery numbers. Watch for the April 2026 Cybercab launch and the first external sales of Optimus, which are currently slated for late 2026 or early 2027. The primary risk remains the enormous CapEx required to build this future; if the global economy faces a significant downturn, Tesla’s $20 billion spending plan could become a liability.

Ultimately, Tesla has doubled down on its CEO’s vision. By aligning itself so closely with xAI and moving away from the legacy car business, Tesla has positioned itself as the premier play on "Physical AI." Whether the market is ready for a world of humanoid workers and driverless cabs remains to be seen, but Tesla has officially set the clock for 2026.

This content is intended for informational purposes only and is not financial advice.