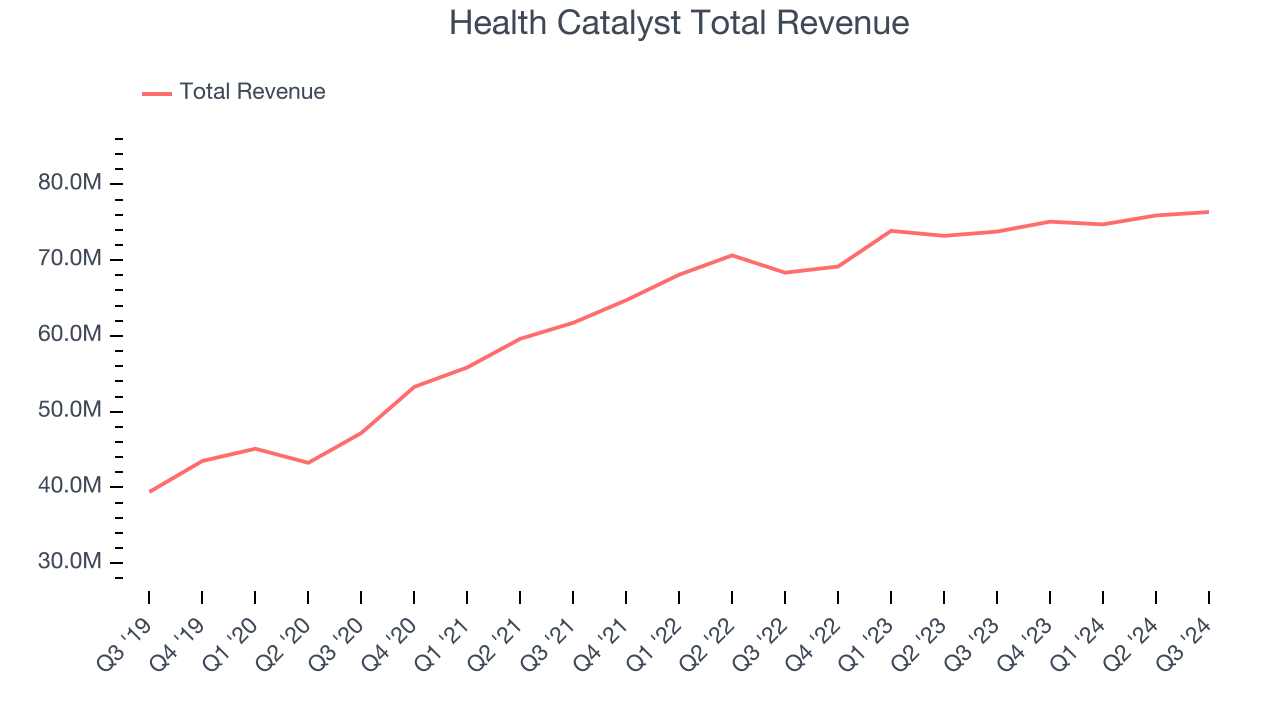

Healthcare software provider Health Catalyst (NASDAQ: HCAT) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 3.5% year on year to $76.35 million. The company expects next quarter’s revenue to be around $81 million, close to analysts’ estimates. Its non-GAAP profit of $0.07 per share was 25.4% below analysts’ consensus estimates.

Is now the time to buy Health Catalyst? Find out by accessing our full research report, it’s free.

Health Catalyst (HCAT) Q3 CY2024 Highlights:

- Revenue: $76.35 million vs analyst estimates of $76.45 million (in line)

- Adjusted EPS: $0.07 vs analyst expectations of $0.09 (25.4% miss)

- Revenue Guidance for Q4 CY2024 is $81 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the full year is $26 million at the midpoint, above analyst estimates of $25.29 million

- Gross Margin (GAAP): 44.6%, up from 43.6% in the same quarter last year

- Operating Margin: -17.9%, up from -33.3% in the same quarter last year

- Free Cash Flow was $1.93 million, up from -$2.44 million in the previous quarter

- Market Capitalization: $469.2 million

“For the third quarter of 2024, I am pleased with our strong financial results, including total revenue of $76.4 million and Adjusted EBITDA of $7.3 million, with these results exceeding the mid-point of our quarterly guidance on each metric. This financial performance continues to demonstrate our ability to scale as we remain focused on driving profitable growth. We are encouraged with our bookings results through Q3 2024 and we are excited to continue this momentum in Q4,” said Dan Burton, CEO of Health Catalyst.

Company Overview

Founded by healthcare professionals Tom Burton and Steve Barlow in 2008, Health Catalyst (NASDAQ: HCAT) provides data and analytics technology to healthcare organizations, enabling them to improve care and lower costs.

Data Analytics

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the siloed data.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Health Catalyst grew its sales at a sluggish 9.4% compounded annual growth rate. This shows it failed to expand in any major way, a rough starting point for our analysis.

This quarter, Health Catalyst grew its revenue by 3.5% year on year, and its $76.35 million of revenue was in line with Wall Street’s estimates. Management is currently guiding for a 7.9% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, similar to its three-year rate. This projection is above the sector average and illustrates the market believes its newer products and services will help maintain its historical top-line performance.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Health Catalyst is very efficient at acquiring new customers, and its CAC payback period checked in at 23.8 months this quarter. The company’s efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving it the freedom to invest resources into new growth initiatives while maintaining optionality.

Key Takeaways from Health Catalyst’s Q3 Results

We were impressed by Health Catalyst’s optimistic EBITDA forecast for next quarter, which blew past analysts’ expectations. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its gross margin declined and its revenue missed Wall Street’s estimates. Overall, we think this was still a decent quarter with some key metrics above expectations. The areas below expectations seem to be driving the move, and shares traded down 4.9% to $7.84 immediately after reporting.

Is Health Catalyst an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.