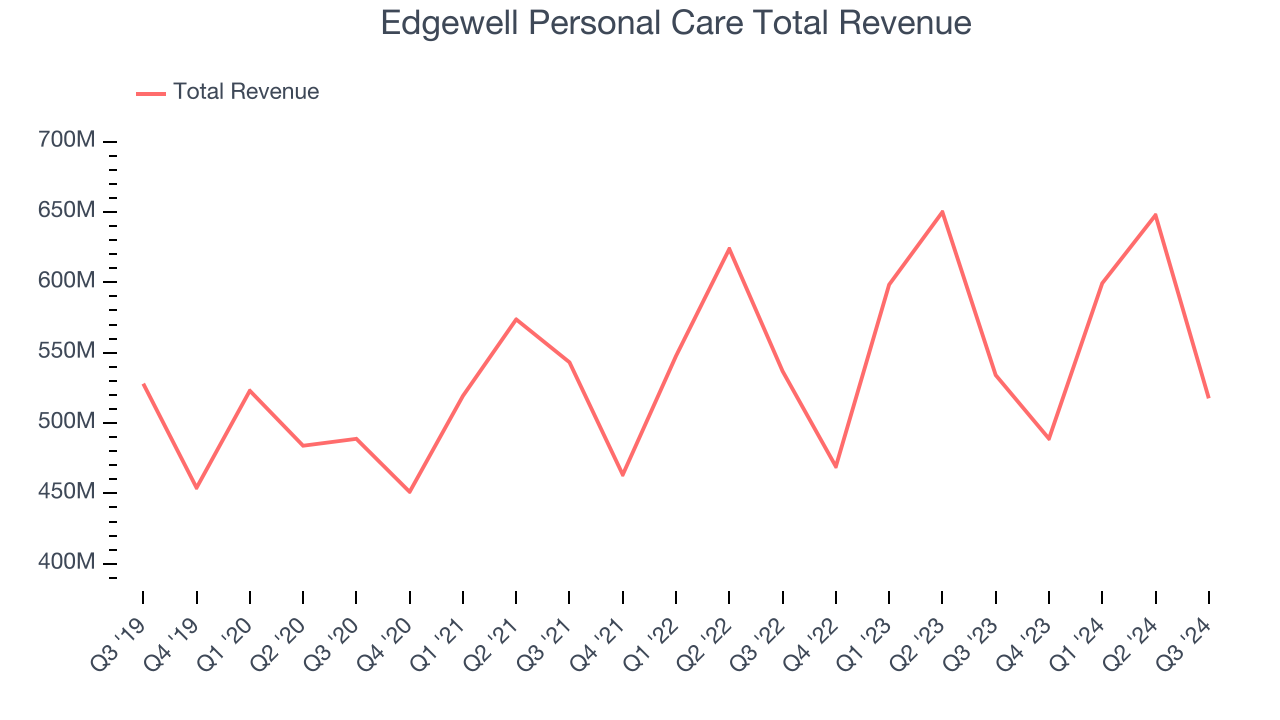

Personal care company Edgewell Personal Care (NYSE: EPC) fell short of the market’s revenue expectations in Q3 CY2024, with sales falling 3.1% year on year to $517.6 million. Its non-GAAP profit of $0.72 per share was 7.7% above analysts’ consensus estimates.

Is now the time to buy Edgewell Personal Care? Find out by accessing our full research report, it’s free.

Edgewell Personal Care (EPC) Q3 CY2024 Highlights:

- Revenue: $517.6 million vs analyst estimates of $535.2 million (3.3% miss)

- Adjusted EPS: $0.72 vs analyst estimates of $0.67 (7.7% beat)

- EBITDA: $78.9 million vs analyst estimates of $82.06 million (3.9% miss)

- Adjusted EPS guidance for the upcoming financial year 2025 is $3.25 at the midpoint, in line with analyst estimates

- EBITDA guidance for the upcoming financial year 2025 is $362 million at the midpoint, below analyst estimates of $376.3 million

- Gross Margin (GAAP): 41.1%, down from 42.6% in the same quarter last year

- Operating Margin: 3.9%, down from 9.6% in the same quarter last year

- EBITDA Margin: 15.2%, in line with the same quarter last year

- Free Cash Flow Margin: 9.2%, up from 5.5% in the same quarter last year

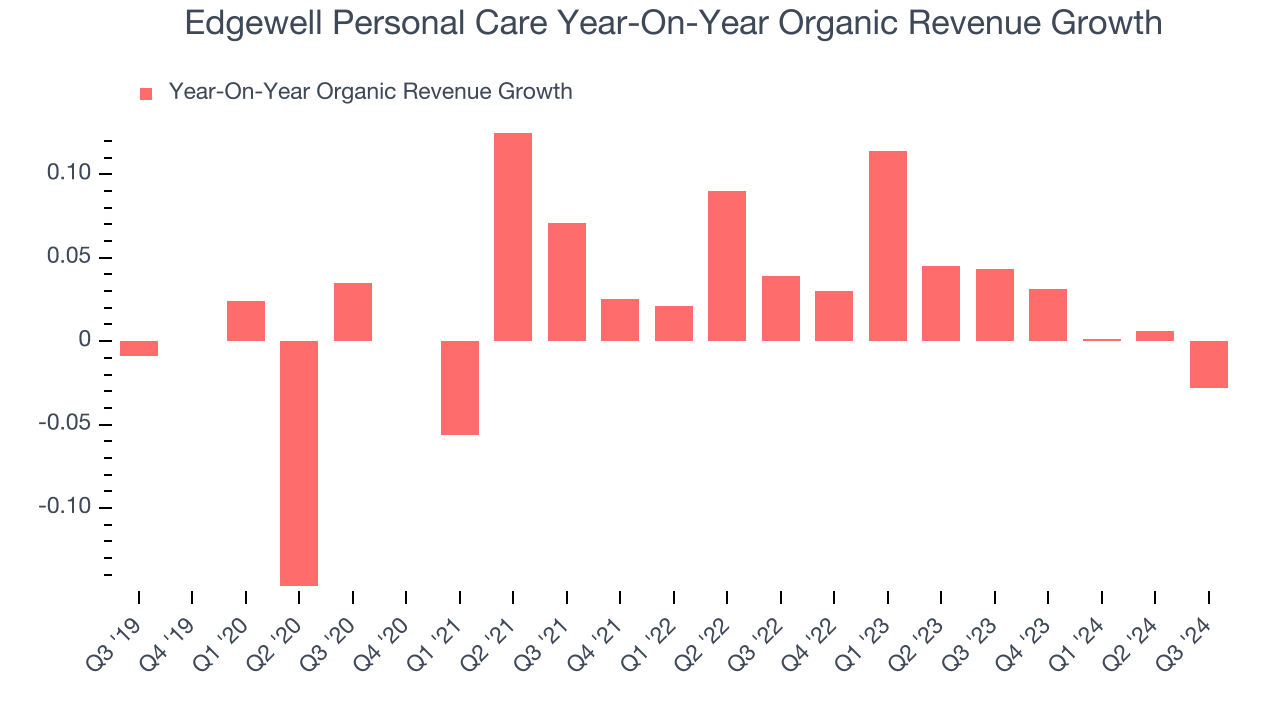

- Organic Revenue fell 2.8% year on year (4.3% in the same quarter last year)

- Market Capitalization: $1.79 billion

"For the fiscal year, we achieved slight organic net sales growth, meaningfully expanded adjusted gross margins and delivered double-digit adjusted earnings per share growth at constant currency for the second consecutive fiscal year. In the face of a heightened competitive landscape and an increasingly cautious consumer, we accelerated organic growth across our international businesses, introduced category-leading innovation in the US Sun Care category and deepened our participation across the men's and women's grooming segments. The strength of our business model was reflected in our healthy earnings growth, substantial cash flow generation and structural de-leveraging of the business," said Rod Little, Edgewell's President and Chief Executive Officer.

Company Overview

Boasting brands such as Banana Boat, Schick, and Skintimate, Edgewell Personal Care (NYSE: EPC) sells personal care products in the skin and sun care, shave, and feminine care categories.

Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

Edgewell Personal Care is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefitting from economies of scale.

As you can see below, Edgewell Personal Care grew its sales at a sluggish 2.6% compounded annual growth rate over the last three years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Edgewell Personal Care missed Wall Street’s estimates and reported a rather uninspiring 3.1% year-on-year revenue decline, generating $517.6 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.6% over the next 12 months, similar to its three-year rate. This projection is underwhelming and shows the market thinks its newer products will not lead to better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding the impacts of foreign currency fluctuations and one-time events such as mergers, acquisitions, and divestitures.

The demand for Edgewell Personal Care’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 3% year on year.

In the latest quarter, Edgewell Personal Care’s organic sales fell 2.8% year on year. This decline was a reversal from the 4.3% year-on-year increase it posted 12 months ago. We’ll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Edgewell Personal Care’s Q3 Results

It was encouraging to see Edgewell Personal Care slightly top analysts’ EPS expectations this quarter. On the other hand, its organic revenue and EBITDA missed Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $36.35 immediately after reporting.

Is Edgewell Personal Care an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.