Earnings results often indicate what direction a company will take in the months ahead. With Q3 behind us, let’s have a look at Freshworks (NASDAQ: FRSH) and its peers.

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

The 4 sales software stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 2.2% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 6.8% on average since the latest earnings results.

Freshworks (NASDAQ: FRSH)

Founded in Chennai, India in 2010 with the idea of creating a “fresh” helpdesk product, Freshworks (NASDAQ: FRSH) offers a broad range of software targeted at small and medium-sized businesses.

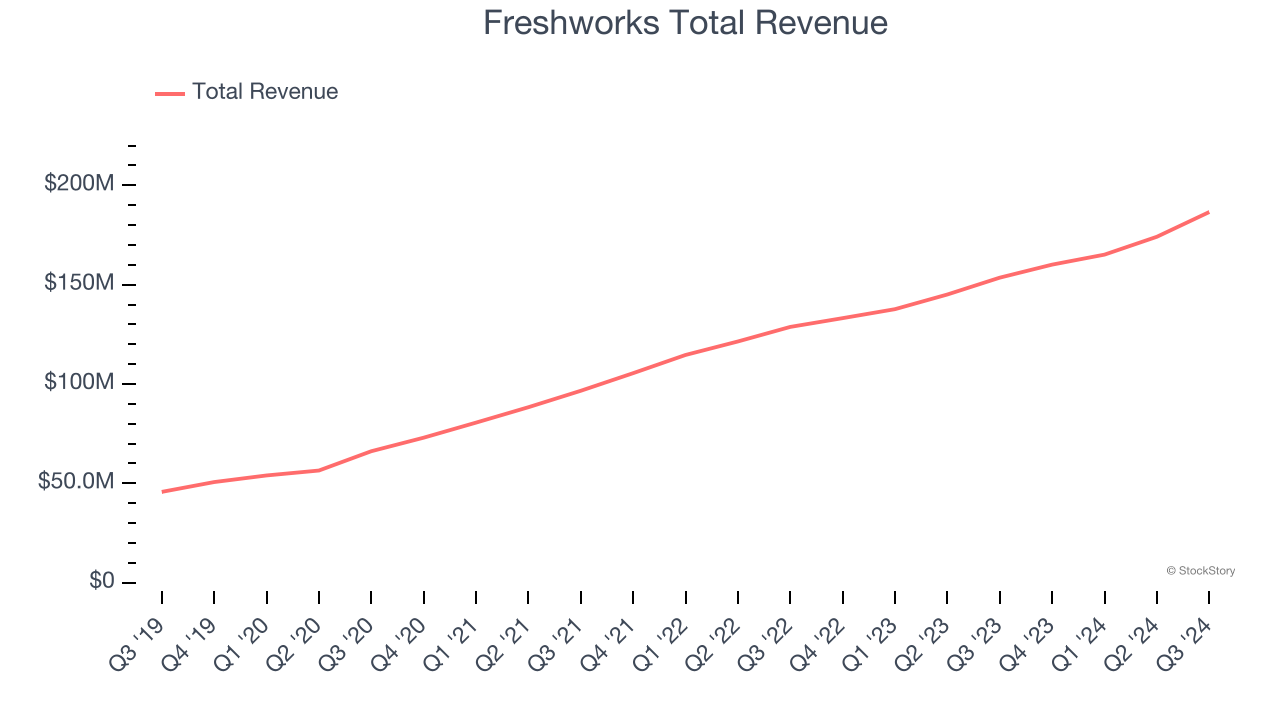

Freshworks reported revenues of $186.6 million, up 21.5% year on year. This print exceeded analysts’ expectations by 2.7%. Overall, it was a strong quarter for the company with a solid beat of analysts’ annual recurring revenue estimates and an impressive beat of analysts’ EBITDA estimates.

“Freshworks delivered a strong third quarter, with revenue growing 22% year over year to $186.6 million, net cash provided by operating activities margin improving to 23%, and free cash flow margin improving to 21%,” said Dennis Woodside, CEO & President of Freshworks.

Freshworks scored the fastest revenue growth of the whole group. The company added 615 enterprise customers paying more than $5,000 annually to reach a total of 22,359. Unsurprisingly, the stock is up 20.3% since reporting and currently trades at $15.75.

We think Freshworks is a good business, but is it a buy today? Read our full report here, it’s free.

Best Q3: HubSpot (NYSE: HUBS)

Started in 2006 by two MIT grad students, HubSpot (NYSE: HUBS) is a software-as-a-service platform that helps small and medium-sized businesses market themselves, sell, and get found on the internet.

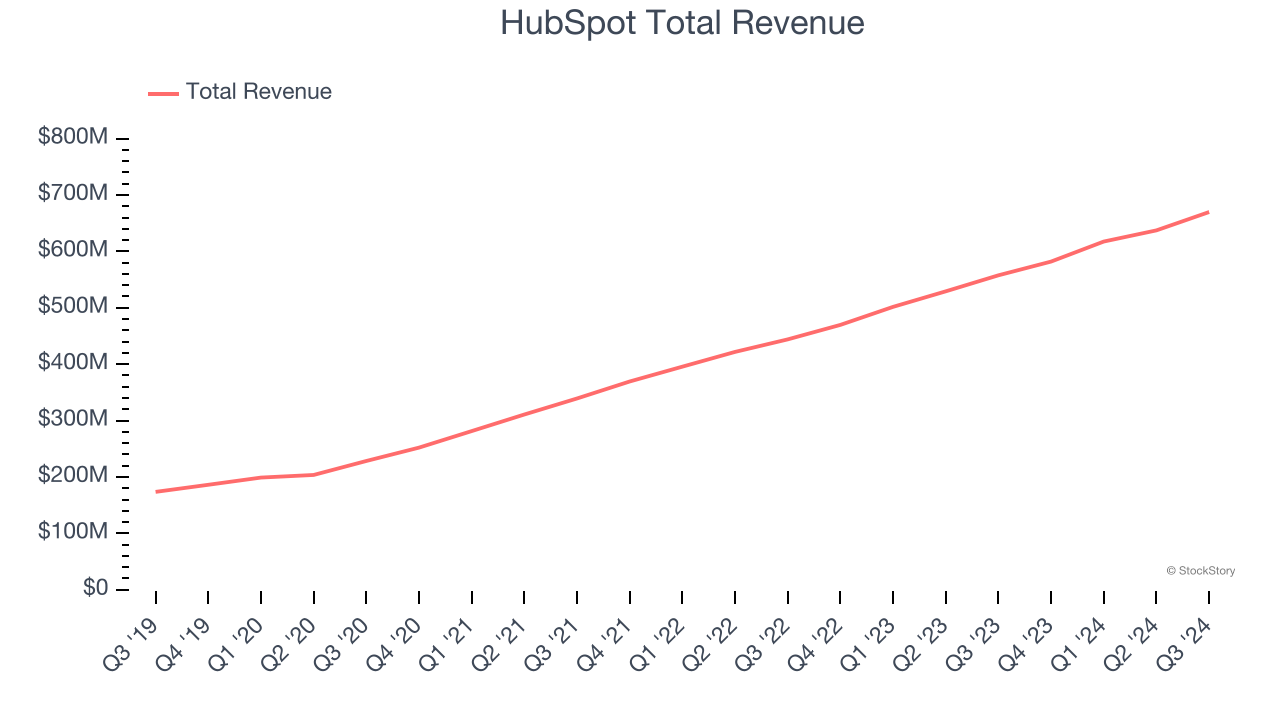

HubSpot reported revenues of $669.7 million, up 20.1% year on year, outperforming analysts’ expectations by 3.5%. The business had a very strong quarter with a solid beat of analysts’ billings estimates and an impressive beat of analysts’ EBITDA estimates.

HubSpot delivered the biggest analyst estimates beat and highest full-year guidance raise among its peers. The company added 10,074 customers to reach a total of 238,128. The market seems happy with the results as the stock is up 20.2% since reporting. It currently trades at $718.99.

Is now the time to buy HubSpot? Access our full analysis of the earnings results here, it’s free.

Slowest Q3: Salesforce (NYSE: CRM)

Launched in 1999 from a rented one-bedroom apartment in San Francisco by Marc Benioff and his three co-founders, Salesforce (NYSE: CRM) is a software-as-a-service platform that helps companies access, manage, and share sales information.

Salesforce reported revenues of $9.44 billion, up 8.3% year on year, exceeding analysts’ expectations by 1%. Still, it was a mixed quarter as it posted revenue and EPS guidance for next quarter missing analysts’ expectations.

Salesforce delivered the weakest performance against analyst estimates and weakest full-year guidance update in the group. Interestingly, the stock is up 3.4% since the results and currently trades at $343.

Read our full analysis of Salesforce’s results here.

ZoomInfo (NASDAQ: ZI)

Founded in 2007 as DiscoveryOrg and renamed after a merger in 2019, ZoomInfo (NASDAQ: ZI) is a software as a service product that provides sales departments with access to a database of prospective clients.

ZoomInfo reported revenues of $303.6 million, down 3.3% year on year. This print topped analysts’ expectations by 1.4%. More broadly, it was a mixed quarter as it also produced full-year EPS guidance exceeding analysts’ expectations but decelerating growth in large customers.

ZoomInfo had the slowest revenue growth among its peers. The company added 12 enterprise customers paying more than $100,000 annually to reach a total of 1,809. The stock is down 16.9% since reporting and currently trades at $10.88.

Read our full, actionable report on ZoomInfo here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% each in November and December), and a notable surge followed Donald Trump's presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by the pace and magnitude of future rate cuts as well as potential changes in trade policy and corporate taxes once the Trump administration takes over. The path forward is marked by uncertainty.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.