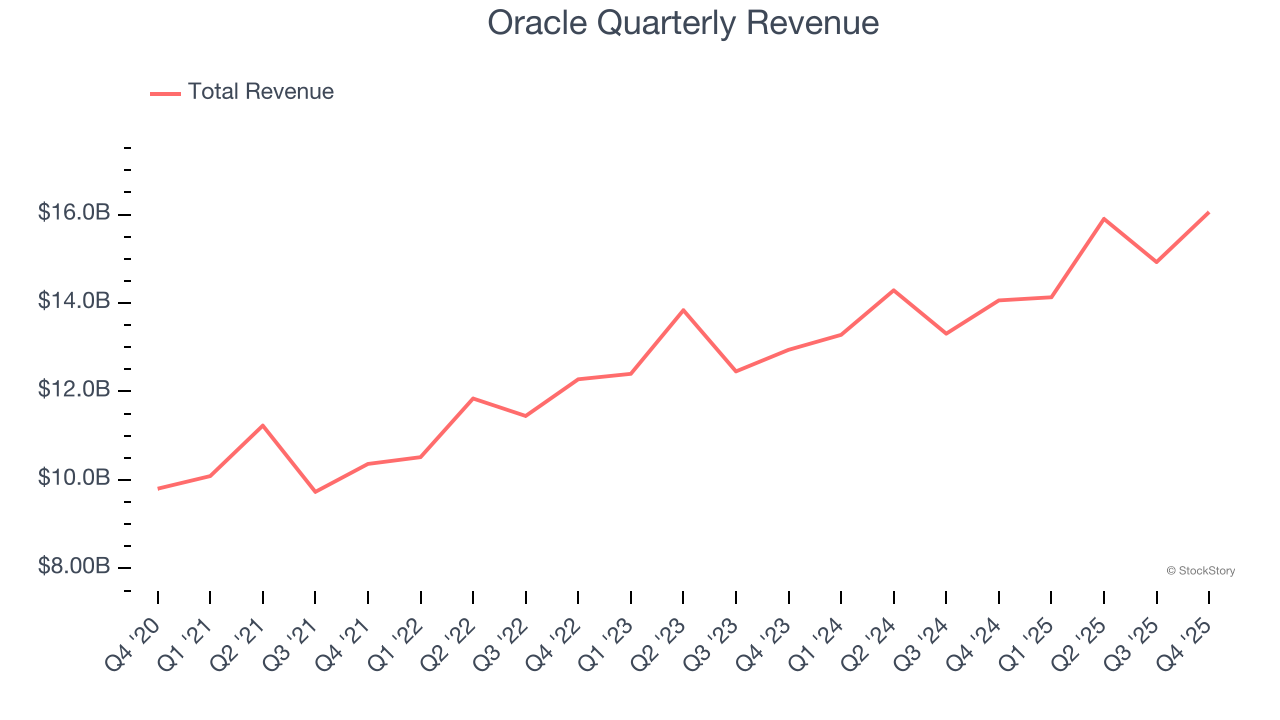

Enterprise software giant Oracle (NYSE: ORCL) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 14.2% year on year to $16.06 billion. Its non-GAAP profit of $2.26 per share was 38% above analysts’ consensus estimates.

Is now the time to buy Oracle? Find out by accessing our full research report, it’s free for active Edge members.

Oracle (ORCL) Q4 CY2025 Highlights:

- Revenue: $16.06 billion vs analyst estimates of $16.19 billion (14.2% year-on-year growth, 0.8% miss)

- Adjusted EPS: $2.26 vs analyst estimates of $1.64 (38% beat)

- Adjusted Operating Income: $6.72 billion vs analyst estimates of $6.81 billion (41.9% margin, 1.3% miss)

- Operating Margin: 29.5%, in line with the same quarter last year

- Free Cash Flow was -$13.18 billion compared to -$362 million in the previous quarter

- Market Capitalization: $631.5 billion

"Oracle is very good at building and running high-performance and cost-efficient cloud datacenters," said Oracle CEO, Clay Magouyrk.

Company Overview

Starting as a database company in 1977 and now powering mission-critical systems across the globe, Oracle (NYSE: ORCL) provides enterprise software and hardware products and services that help businesses manage their information technology needs.

Revenue Growth

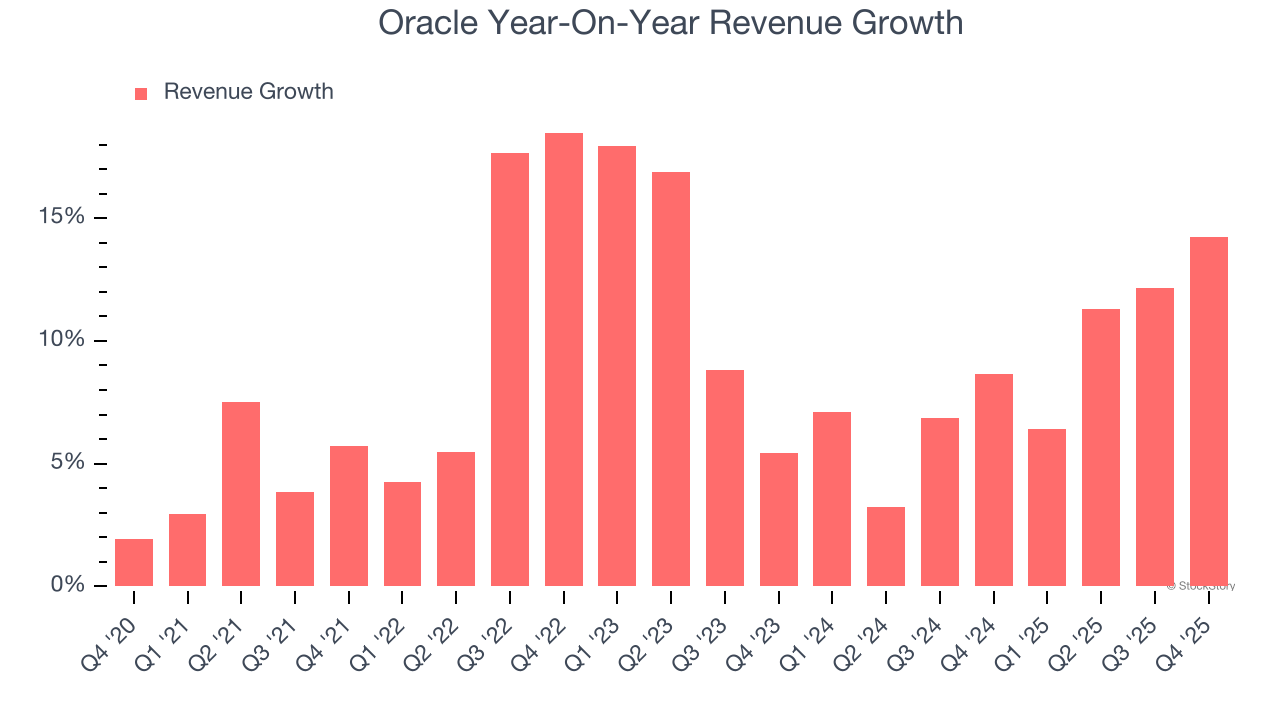

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Oracle grew its sales at a sluggish 9.1% compounded annual growth rate. This was below our standard for the software sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Oracle’s annualized revenue growth of 8.7% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Oracle’s revenue grew by 14.2% year on year to $16.06 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 21.8% over the next 12 months, an improvement versus the last two years. This projection is particularly noteworthy for a company of its scale and implies its newer products and services will spur better top-line performance.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

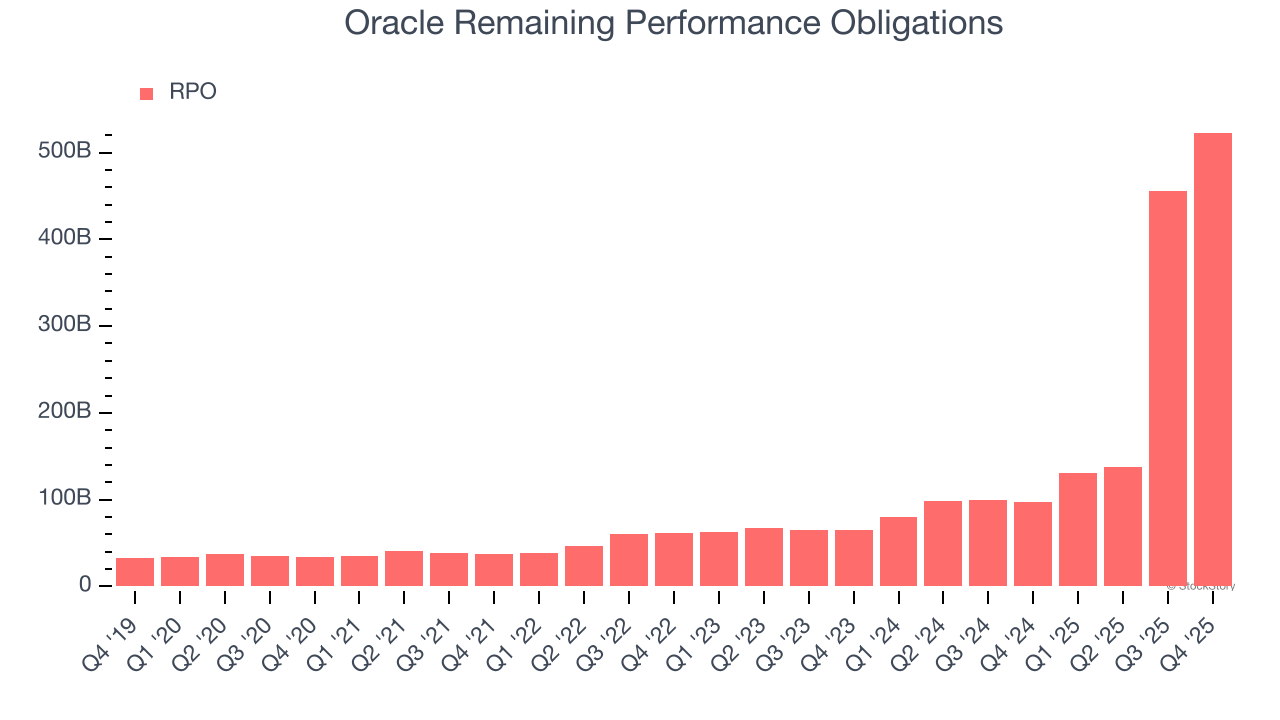

Remaining Performance Obligations

In addition to reported revenue, it is useful to analyze RPO, or remaining performance obligations, for Oracle because it shows the value of contracted services to be delivered in the future. It therefore gives visibility into future revenue.

Oracle’s RPO punched in at $523 billion in Q4, and over the last four quarters, its growth was fantastic as it averaged 225% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means contracted services not yet delivered are growing faster than services already delivered (the criteria for revenue recognition). That could be a good sign for future revenue growth.

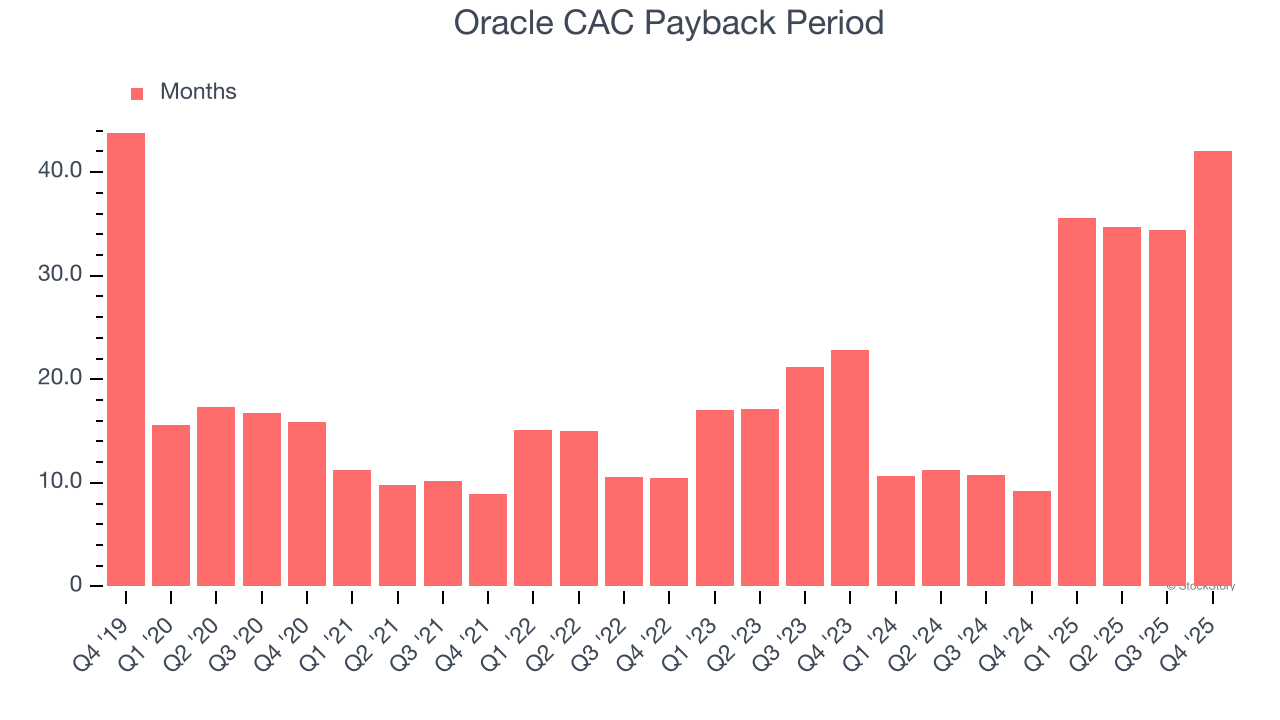

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Oracle is efficient at acquiring new customers, and its CAC payback period checked in at 42.1 months this quarter. The company’s relatively fast recovery of its customer acquisition costs gives it the option to accelerate growth by increasing its sales and marketing investments.

Key Takeaways from Oracle’s Q4 Results

We struggled to find many positives in these results. Its revenue slightly missed and its remaining performance obligation fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5.3% to $211.95 immediately after reporting.

Oracle didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.