Wrapping up Q3 earnings, we look at the numbers and key takeaways for the building materials stocks, including Carlisle (NYSE: CSL) and its peers.

Traditionally, building materials companies have built competitive advantages with economies of scale, brand recognition, and strong relationships with builders and contractors. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of building materials companies.

The 8 building materials stocks we track reported a slower Q3. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 1.1% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.6% since the latest earnings results.

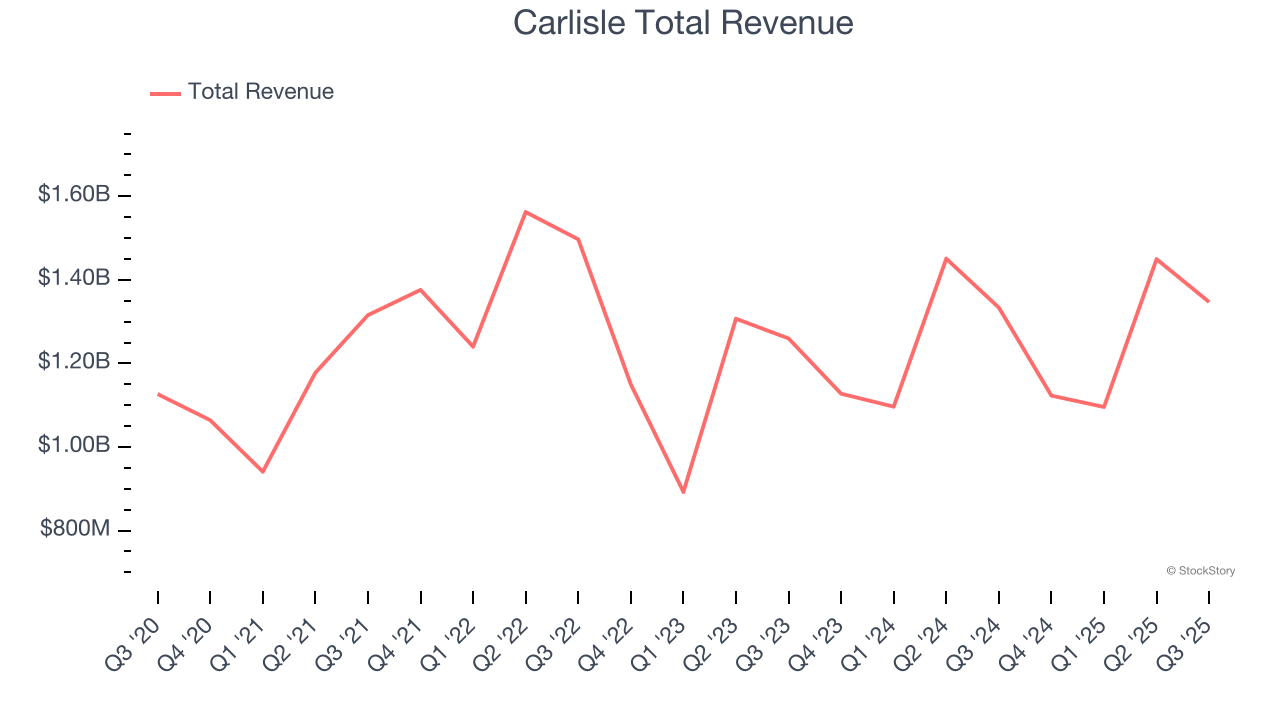

Best Q3: Carlisle (NYSE: CSL)

Originally founded as Carlisle Tire and Rubber Company, Carlisle Companies (NYSE: CSL) is a multi-industry product manufacturer focusing on construction materials and weatherproofing technologies.

Carlisle reported revenues of $1.35 billion, flat year on year. This print exceeded analysts’ expectations by 1.2%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ adjusted operating income and organic revenue estimates.

Unsurprisingly, the stock is down 3.5% since reporting and currently trades at $319.65.

Is now the time to buy Carlisle? Access our full analysis of the earnings results here, it’s free for active Edge members.

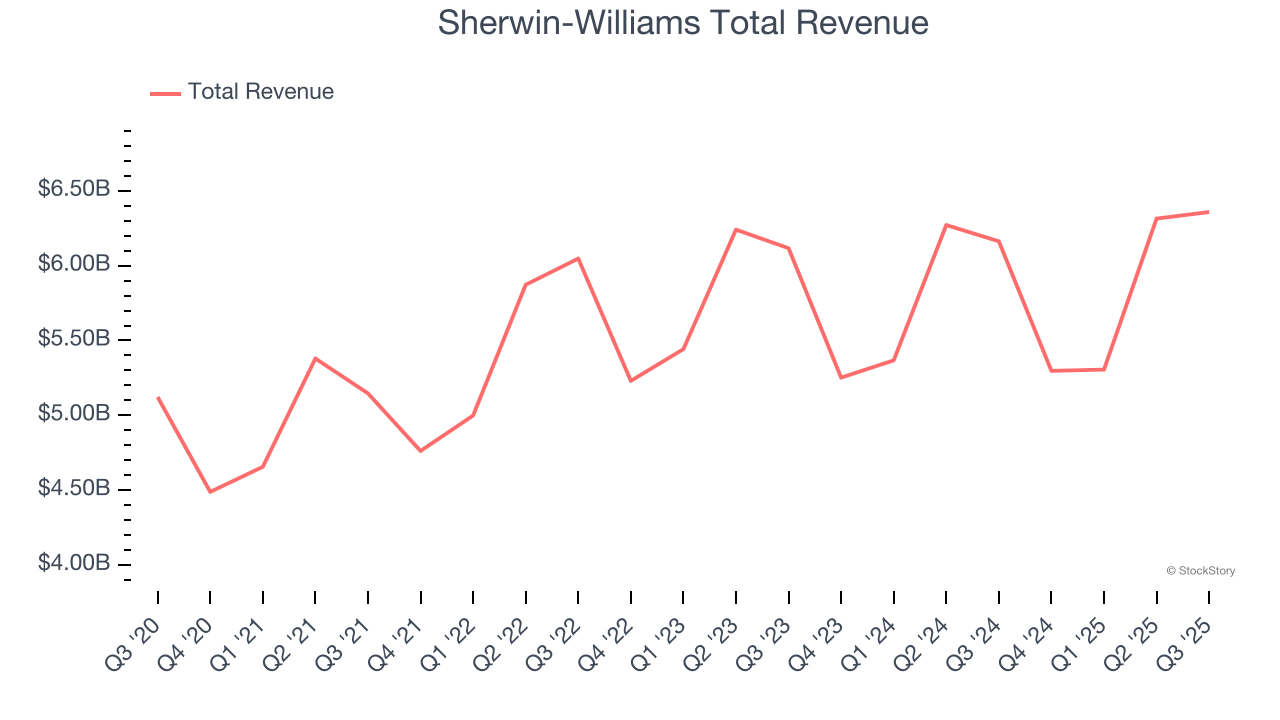

Sherwin-Williams (NYSE: SHW)

Widely known for its success in the paint industry, Sherwin-Williams (NYSE: SHW) is a manufacturer of paints, coatings, and related products.

Sherwin-Williams reported revenues of $6.36 billion, up 3.2% year on year, outperforming analysts’ expectations by 2.6%. The business had a strong quarter with an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ revenue estimates.

Sherwin-Williams scored the biggest analyst estimates beat among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $337.41.

Is now the time to buy Sherwin-Williams? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Tecnoglass (NYSE: TGLS)

The first-ever Colombian company to trade on the NASDAQ, Tecnoglass (NYSE: TGLS) is a manufacturer of architectural glass, windows, and aluminum products.

Tecnoglass reported revenues of $260.5 million, up 9.3% year on year, falling short of analysts’ expectations by 2.1%. It was a disappointing quarter as it posted full-year EBITDA guidance missing analysts’ expectations significantly and a significant miss of analysts’ revenue estimates.

As expected, the stock is down 10.7% since the results and currently trades at $50.03.

Read our full analysis of Tecnoglass’s results here.

UFP Industries (NASDAQ: UFPI)

Beginning as a lumber supplier in the 1950s, UFP Industries (NASDAQ: UFPI) is a holding company making building materials for the construction, retail, and industrial sectors.

UFP Industries reported revenues of $1.56 billion, down 5.4% year on year. This result missed analysts’ expectations by 3.2%. Overall, it was a disappointing quarter as it also logged a significant miss of analysts’ revenue estimates and a significant miss of analysts’ adjusted operating income estimates.

UFP Industries had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is flat since reporting and currently trades at $90.40.

Read our full, actionable report on UFP Industries here, it’s free for active Edge members.

Vulcan Materials (NYSE: VMC)

Founded in 1909, Vulcan Materials (NYSE: VMC) is a producer of construction aggregates, primarily crushed stone, sand, and gravel.

Vulcan Materials reported revenues of $2.29 billion, up 14.4% year on year. This print beat analysts’ expectations by 0.8%. More broadly, it was a satisfactory quarter as it also produced a decent beat of analysts’ adjusted operating income estimates but full-year EBITDA guidance slightly missing analysts’ expectations.

Vulcan Materials pulled off the fastest revenue growth among its peers. The stock is down 1.8% since reporting and currently trades at $289.63.

Read our full, actionable report on Vulcan Materials here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.