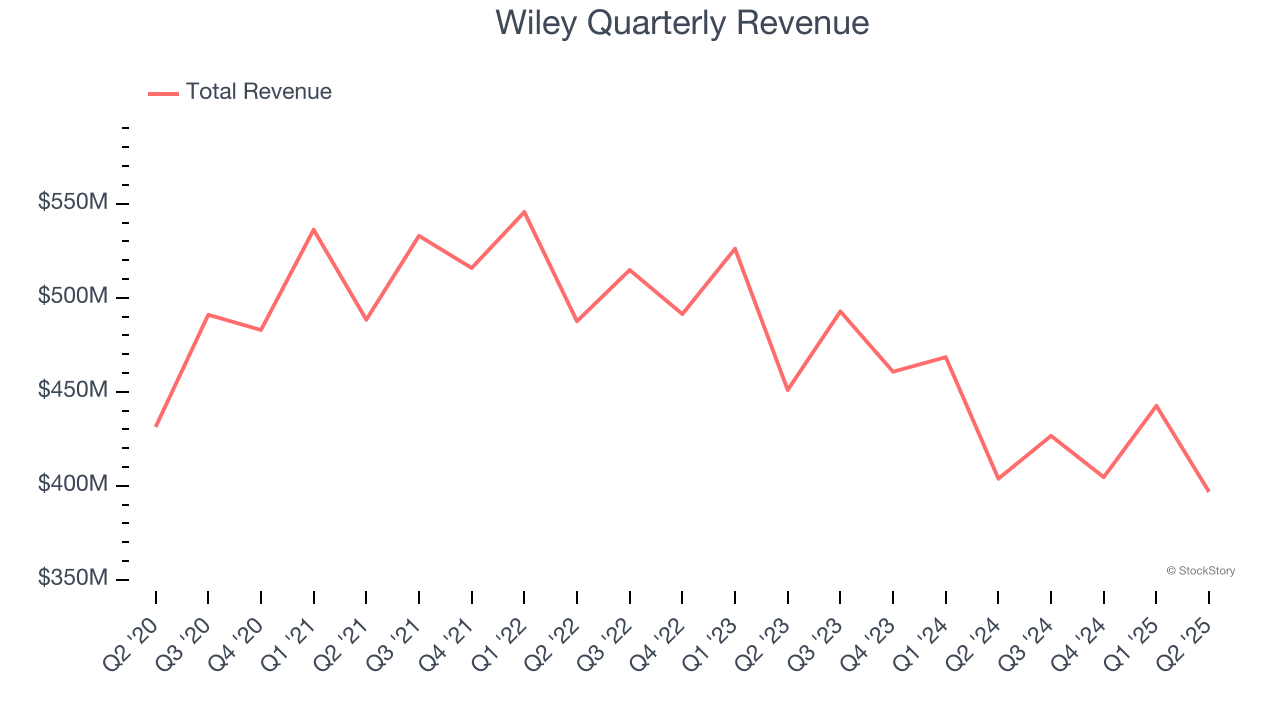

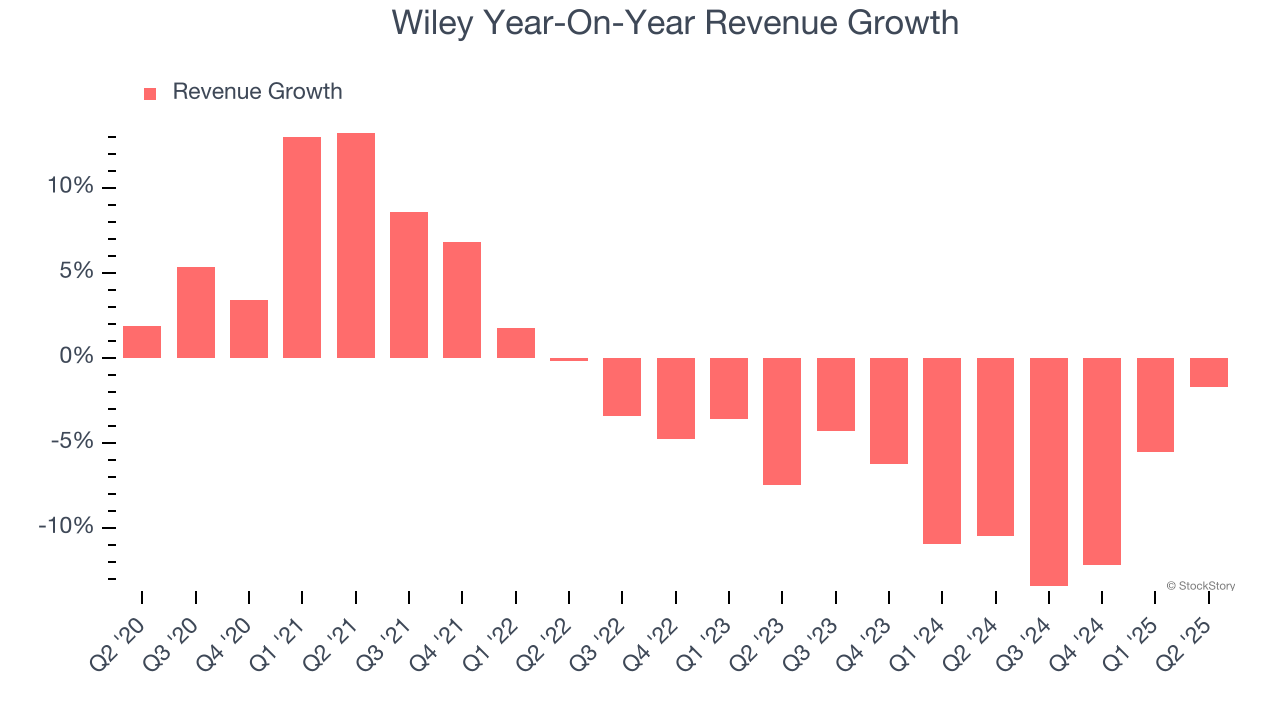

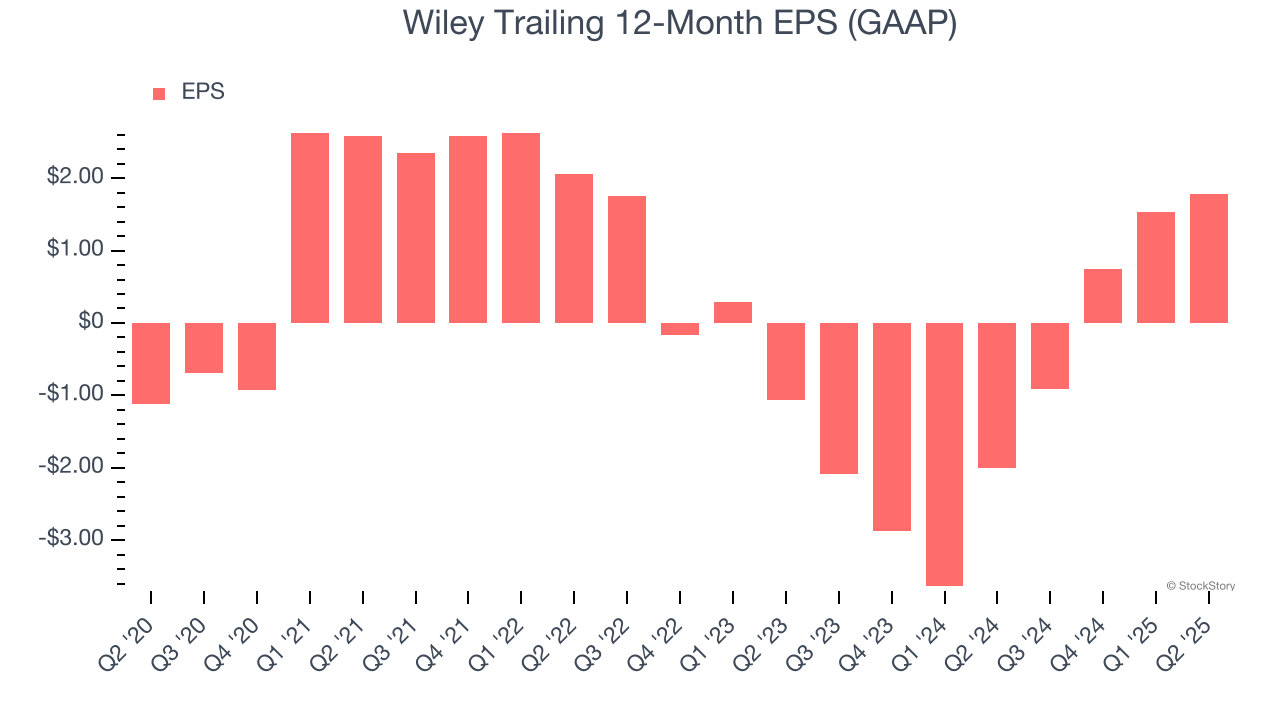

Academic publishing company John Wiley & Sons (NYSE: WLY) posted $396.8 million of revenue in Q2 CY2025, down 1.7% year on year. Its GAAP profit of $0.22 per share increased from -$0.03 in the same quarter last year.

Is now the time to buy Wiley? Find out by accessing our full research report, it’s free.

Wiley (WLY) Q2 CY2025 Highlights:

- Revenue: $396.8 million (1.7% year-on-year decline)

- Adjusted EBITDA: $70.45 million (17.8% margin, 3% year-on-year decline)

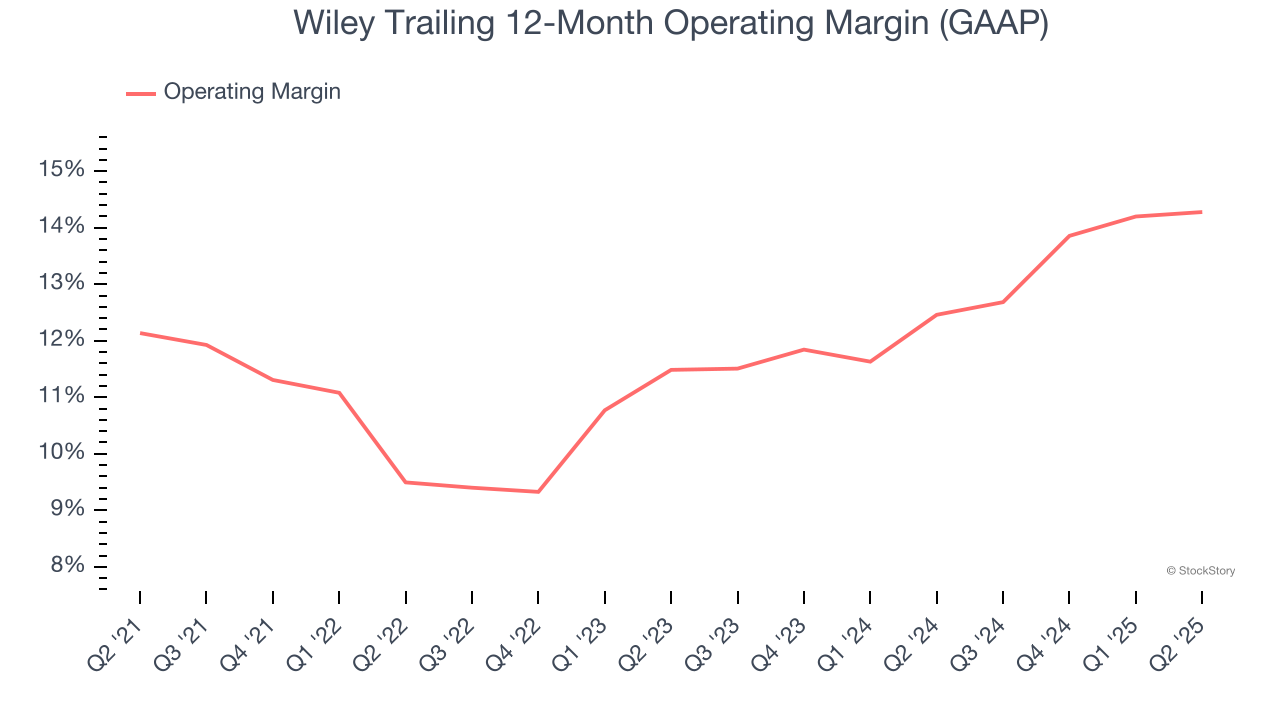

- Operating Margin: 7.8%, in line with the same quarter last year

- Free Cash Flow was -$99.9 million compared to -$103.2 million in the same quarter last year

- Market Capitalization: $2.12 billion

“We continue to see strong demand trends in research as we open up new growth pathways in AI and corporate R&D,” said Matthew Kissner, President and CEO.

Company Overview

With roots dating back to 1807 when Charles Wiley opened a small printing shop in Manhattan, John Wiley & Sons (NYSE: WLY) is a global academic publisher that provides scientific journals, books, digital courseware, and knowledge solutions for researchers, students, and professionals.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.67 billion in revenue over the past 12 months, Wiley is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Wiley’s demand was weak over the last five years. Its sales fell by 1.9% annually, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Wiley’s recent performance shows its demand remained suppressed as its revenue has declined by 8.2% annually over the last two years.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Wiley has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 11.9%, higher than the broader business services sector.

Looking at the trend in its profitability, Wiley’s operating margin rose by 2.1 percentage points over the last five years, showing its efficiency has improved.

This quarter, Wiley generated an operating margin profit margin of 7.8%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Wiley’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Wiley, its two-year annual EPS growth of 91.8% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q2, Wiley reported EPS of $0.22, up from negative $0.03 in the same quarter last year. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Wiley’s Q2 Results

We struggled to find many positives in these results. Overall, this was a weaker quarter. The stock remained flat at $40 immediately after reporting.

Big picture, is Wiley a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.