Over the last six months, Aramark’s shares have sunk to $38.93, producing a disappointing 10.8% loss - a stark contrast to the S&P 500’s 10.4% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Aramark, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Aramark Not Exciting?

Even though the stock has become cheaper, we're swiping left on Aramark for now. Here are three reasons there are better opportunities than ARMK and a stock we'd rather own.

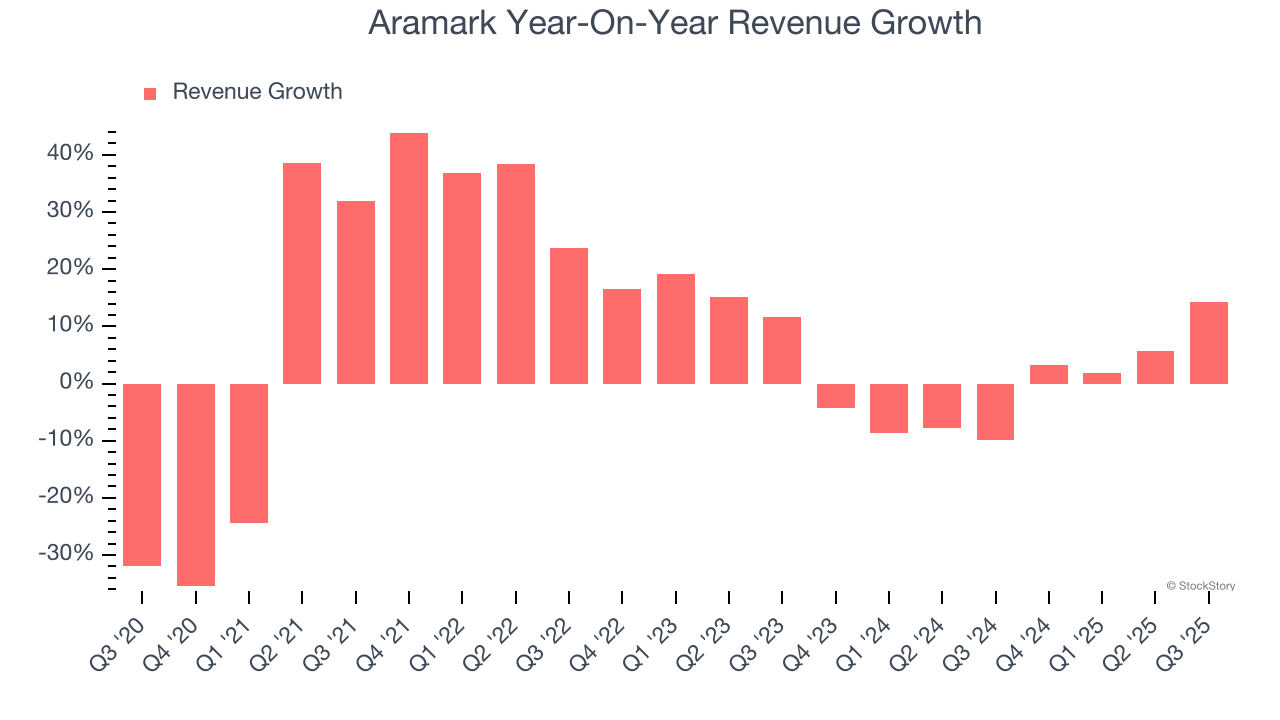

1. Revenue Growth Flatlining

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. Aramark’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

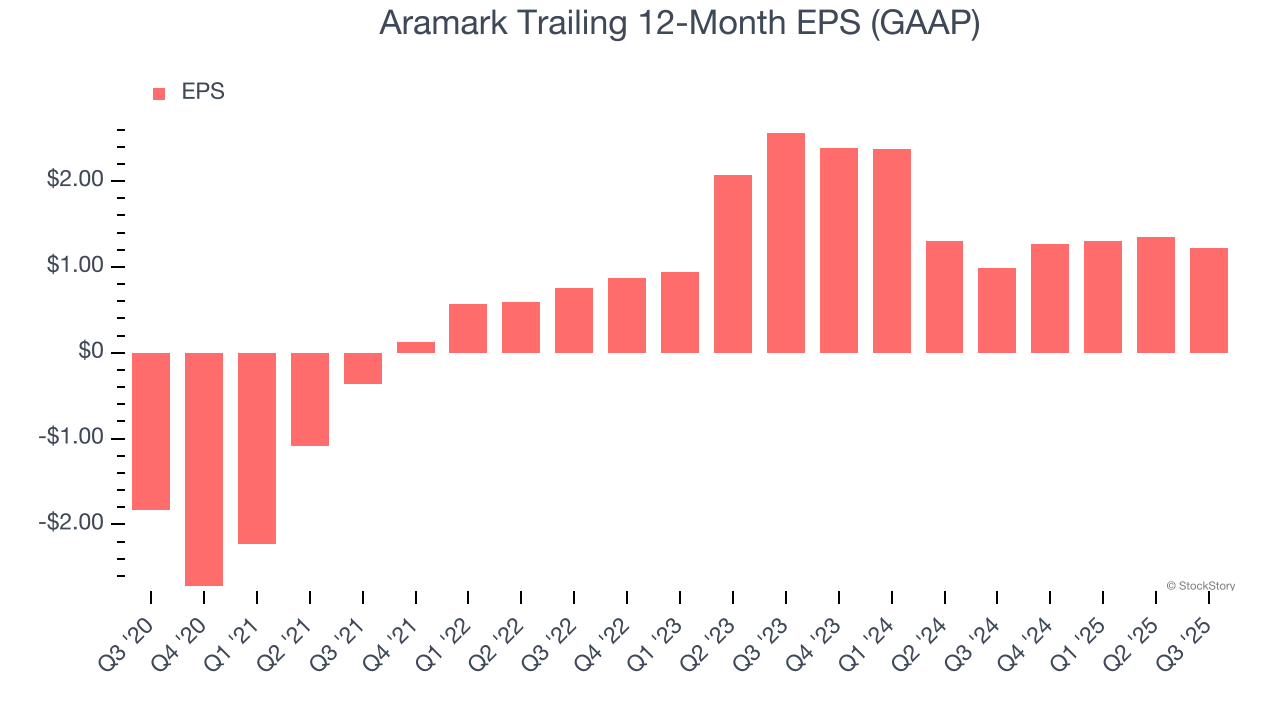

2. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Aramark, its EPS declined by 31% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

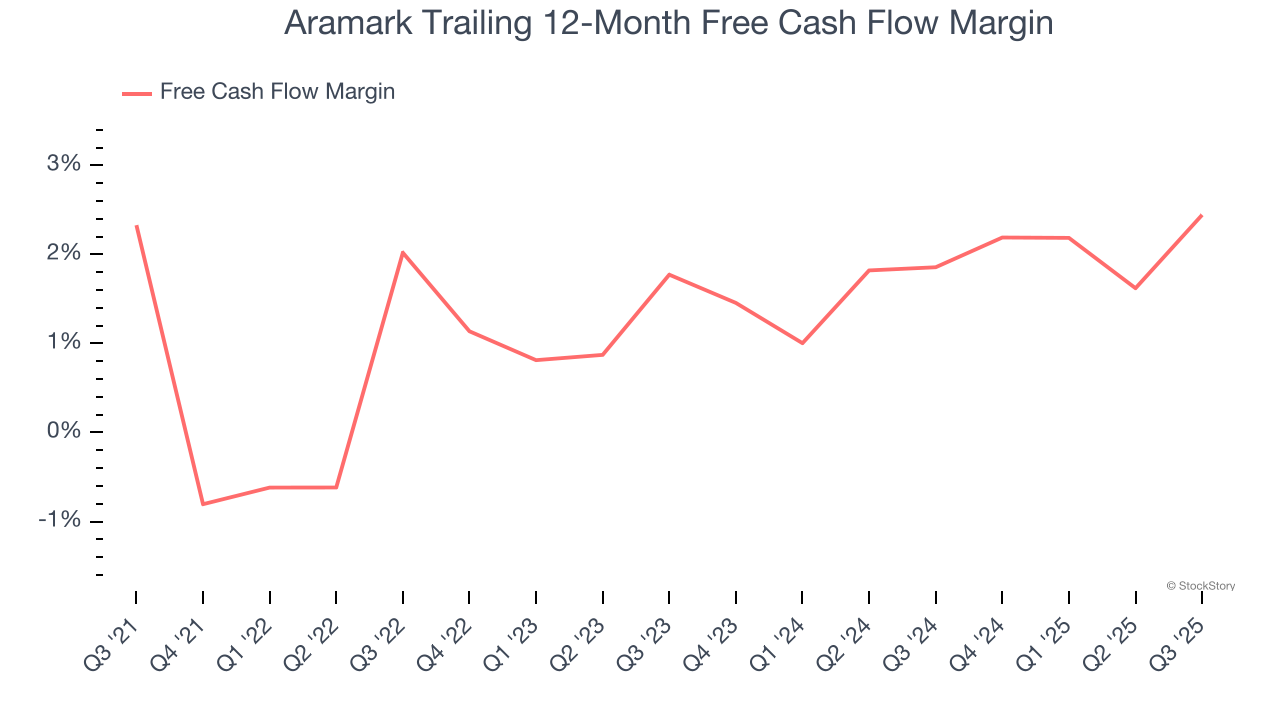

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Aramark has shown poor cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.1%, lousy for a business services business.

Final Judgment

Aramark isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 17.6× forward P/E (or $38.93 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Aramark

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.