Let’s dig into the relative performance of JELD-WEN (NYSE: JELD) and its peers as we unravel the now-completed Q3 home construction materials earnings season.

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

The 12 home construction materials stocks we track reported a slower Q3. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 0.5% below.

In light of this news, share prices of the companies have held steady as they are up 2.1% on average since the latest earnings results.

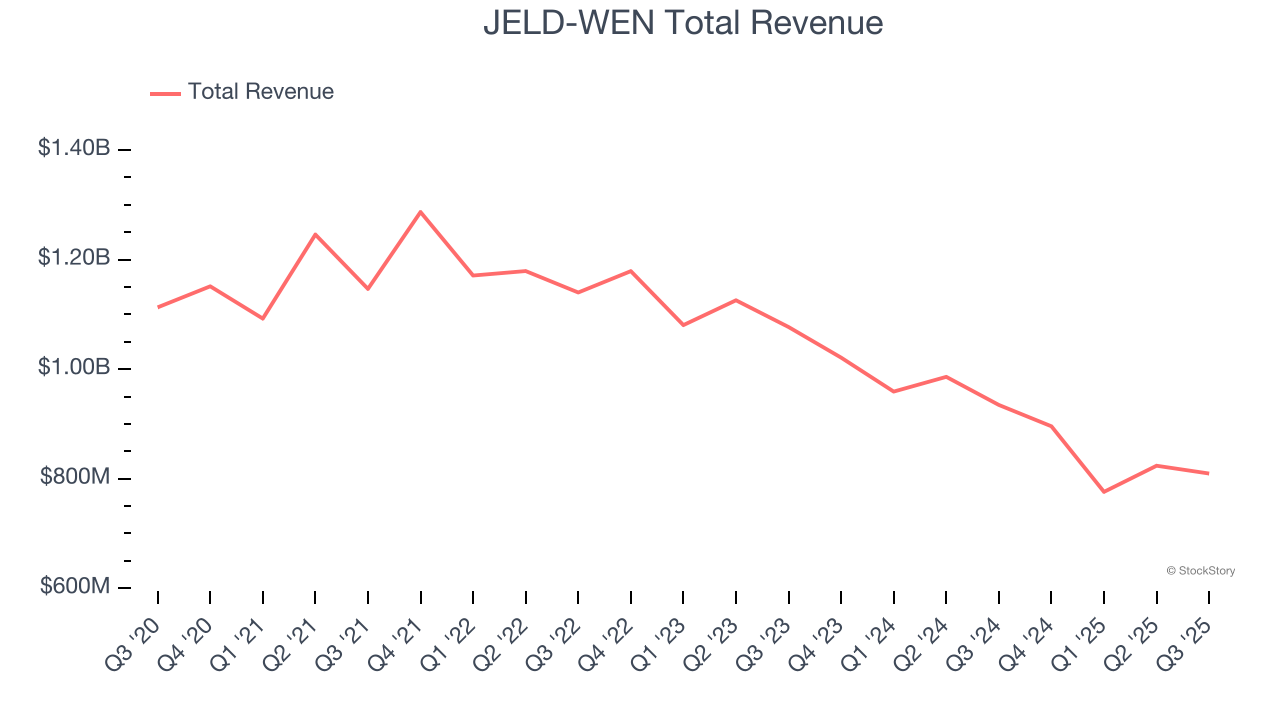

JELD-WEN (NYSE: JELD)

Founded in the 1960s as a general wood-making company, JELD-WEN (NYSE: JELD) manufactures doors, windows, and other related building products.

JELD-WEN reported revenues of $809.5 million, down 13.4% year on year. This print fell short of analysts’ expectations by 2%. Overall, it was a disappointing quarter for the company with full-year EBITDA guidance missing analysts’ expectations and a significant miss of analysts’ adjusted operating income estimates.

"Third-quarter results fell short of our expectations due to persistent market headwinds and price-cost pressures," said Chief Executive Officer William J. Christensen.

JELD-WEN delivered the slowest revenue growth of the whole group. Unsurprisingly, the stock is down 33.8% since reporting and currently trades at $2.78.

Read our full report on JELD-WEN here, it’s free.

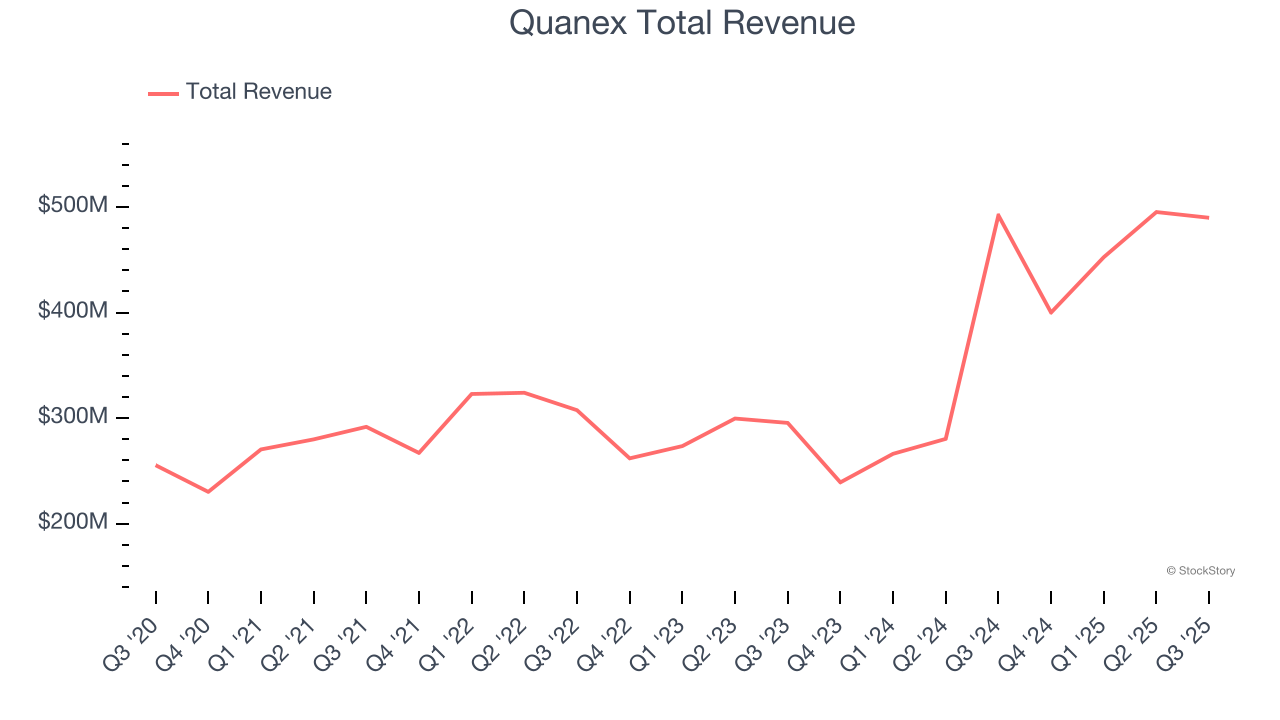

Best Q3: Quanex (NYSE: NX)

Starting in the seamless tube industry, Quanex (NYSE: NX) manufactures building products like window, door, kitchen, and bath cabinet components.

Quanex reported revenues of $489.8 million, flat year on year, outperforming analysts’ expectations by 4.4%. The business had an incredible quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems happy with the results as the stock is up 16.3% since reporting. It currently trades at $17.54.

Is now the time to buy Quanex? Access our full analysis of the earnings results here, it’s free.

American Woodmark (NASDAQ: AMWD)

Starting as a small millwork shop, American Woodmark (NASDAQ: AMWD) is a cabinet manufacturing company that helps customers from inspiration to installation.

American Woodmark reported revenues of $394.6 million, down 12.8% year on year, falling short of analysts’ expectations by 2.4%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ adjusted operating income estimates.

Interestingly, the stock is up 15.7% since the results and currently trades at $59.99.

Read our full analysis of American Woodmark’s results here.

Masco (NYSE: MAS)

Headquartered just outside of Detroit, MI, Masco (NYSE: MAS) designs and manufactures home-building products such as glass shower doors, decorative lighting, bathtubs, and faucets.

Masco reported revenues of $1.92 billion, down 3.3% year on year. This result lagged analysts' expectations by 1.5%. Overall, it was a disappointing quarter as it also logged a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EBITDA estimates.

The stock is up 1.3% since reporting and currently trades at $69.32.

Read our full, actionable report on Masco here, it’s free.

Simpson (NYSE: SSD)

Aiming to build safer and stronger buildings, Simpson (NYSE: SSD) designs and manufactures structural connectors, anchors, and other construction products.

Simpson reported revenues of $623.5 million, up 6.2% year on year. This print beat analysts’ expectations by 3.1%. Aside from that, it was a slower quarter as it logged a significant miss of analysts’ EPS and EBITDA estimates.

The stock is up 1.8% since reporting and currently trades at $179.03.

Read our full, actionable report on Simpson here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.